In a shortened holiday week, U.S. stock markets closed with losses primarily due to an upward shift in the interest rate outlook, driven by positive economic signals. Apple, a significant component of the S&P 500, saw a decline, attributed to reports of Chinese government employees discontinuing iPhone usage and concerns regarding the upcoming iPhone 15. NVIDIA and other chip manufacturers also contributed to the market’s challenges.

Despite these hurdles, the economic calendar for the week delivered positive news. The Institute for Supply Management reported that August’s services sector activity reached its highest level since February, surprising analysts. New orders displayed robust growth, although order backlogs witnessed a significant drop. Export orders remained healthy, although concerns arose regarding a potential slowdown in the Chinese economy.

The U.S. also reported weekly jobless claims that exceeded expectations. Despite a minor increase in the August unemployment rate, the number of Americans seeking unemployment benefits hit a six-month low, accompanied by a reduction in ongoing claims.

In the Eurozone, there was a downward revision of Q2 GDP growth to 0.1%, a decrease from the initial estimate of a 0.3% expansion. This revision was largely due to a decline in exports, highlighting the region’s economic challenges.

The UK experienced declines in its services PMI and house price index. The Halifax house price index recorded a significant 1.9% month-over-month decline in August. Bank of England (BoE) Governor Andrew Bailey hinted at a potential shift in the central bank’s interest rate policy, expressing uncertainty about an imminent rate hike at the September 21 policy meeting. Bailey emphasized the need for a more nuanced decision-making process.

In China, economic concerns led to declines in Chinese stocks, while the services sector showed signs of slowing. Exports and imports contracted but exceeded expectations. China’s renminbi currency hit a record low against the U.S. dollar, reflecting economic uncertainties. In other China-related developments, authorities are contemplating expanding the ban on iPhones’ use in sensitive departments, government-backed agencies, and state-owned enterprises as part of a broader effort to restrict foreign technology usage in sensitive environments.

Japan’s GDP growth slightly missed expectations. Speculation swirled about a potential political reshuffle within the Liberal Democratic Party.

On a global scale, Copernicus confirmed record-breaking summer heatwaves, highlighting the urgent need to address climate change. Extreme temperatures affected North America, Europe, and Asia, underscoring the imperative to reduce greenhouse gas emissions.

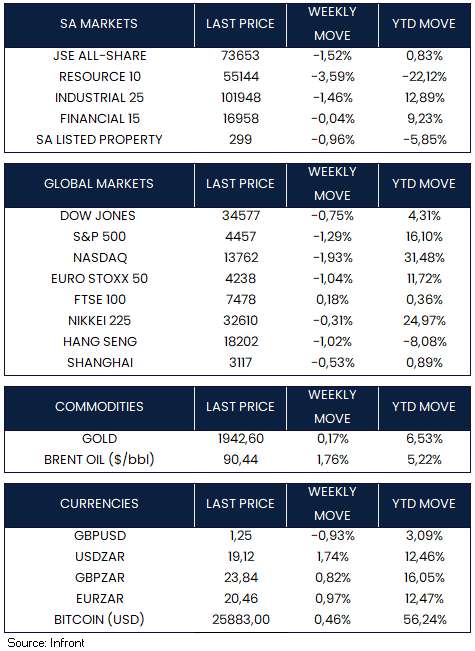

Global equity markets concluded the week with losses. In the U.S., the Dow Jones (-0.75%), S&P 500 (-1.29%), and Nasdaq (-1.93%) all closed the week in the red. Similarly, European and Asian markets, including the Euro Stoxx 50 (-1.04%), Nikkei 225 (-0.31%), Hang Seng (-1.02%) and Shanghai (-0.53%) indices, experienced declines, with the FTSE 100 Index (+0.18%) being the exception.

Market Moves of the Week:

SA’s economy showed some resilience, with GDP increasing from +0.4% QoQ in Q1 to +0.6% QoQ in Q2. Growth exceeded consensus and SARB forecasts, fuelled by a significant increase in private sector fixed investment, despite a drop in household consumption. At the same time, SA’s current account deficit increased from 0.9% of GDP in Q1 2023 to 2.3% in Q2, less severe than expected.

Nevertheless, National Treasury faces significant challenges amid shrinking tax revenue and mounting debt. SA’s budget deficit reached R143.8 billion in July, the largest since 2004, with the debt-to-GDP ratio at 73% and potentially reaching 80% by end-2024. Finance Minister Enoch Godongwana has subsequently hinted at potential tax increases to address revenue shortfalls but acknowledged limitations due to ongoing tax collection underperformance. Budget cuts were also highlighted as an option, but less likely in an election year.

The JSE All-Share Index (-1.52%) was negative this week. Weaker performances came from the resource (-3.59%) and industrial (-1.46%) sectors, while the financial sector (-0.04%) was largely unchanged. By Friday close, the rand was trading at R19.12 to the U.S. Dollar, depreciating by -1.74% for the week.

Chart of the Week:

Amid ongoing negative developments in China, the world’s second-largest economy faces an uncertain future. The $18 trillion economy is slowing down, with low consumer sentiment, export challenges, price deflation, and a youth unemployment rate exceeding 20%. Bloomberg Economics predicts that China may not surpass the U.S. in gross domestic product until the mid-2040s. This represents a significant departure from pre-pandemic expectations, where China was anticipated to secure and maintain the top spot as early as the beginning of the next decade.

Source: Bloomberg