Monthly Update

September 2025

Market Snapshot: Growth Momentum Intact as Policy Easing Nears

Global markets ended the third quarter on a constructive note, with September extending the gains seen across most major indices this year. Investor sentiment was supported by moderating inflation, resilient economic activity, and growing conviction that the next stage of the cycle will be defined by gradual monetary easing. The MSCI All-Country World Index advanced 3.6% in September and is now up 7.6% for Q3, with developed and emerging markets both positive.

In the U.S., softer labour data and dovish commentary reinforced expectations of a Fed cut before yearend. In Europe, political and fiscal uncertainty capped enthusiasm, but equities still managed to advance. Japan and U.S. technology shares outperformed strongly, supported by gains in Chinese tech, while the broader mainland Chinese market lagged as property and consumption headwinds persisted despite renewed stimulus efforts.

Commodities diverged, with gold surging to new record highs on safe-haven flows while oil stabilised after prior weakness. South Africa posted another standout month, with the JSE All Share gaining nearly 6% – its seventh consecutive advance – driven overwhelmingly by resources. The rand strengthened alongside firm commodity inflows.

Key Trends This Month:

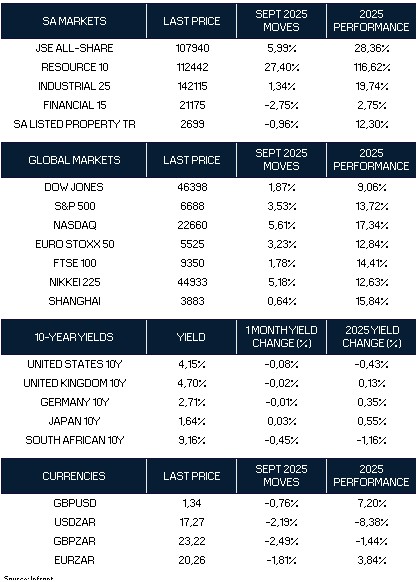

- Global equities higher; Nasdaq (+5.6%), Nikkei (+5.2%), and S&P 500 (+3.5%) led.

- Europe steady; Euro Stoxx 50 (+3.2%) outperformed FTSE 100 (+1.8%).

- Mainland China lagged, with Shanghai up only +0.6%.

- South Africa’s Resource 10 surged +27.4%, while financials (−2.8%) and property (−1.0%) fell.

- Global bond yields declined, except in Japan.

- The rand gained +2.2% vs USD, supported by risk-on sentiment and commodity inflows.

United States: Earnings Resilient, Fed Pivot Anticipated

Equity Performance:

- Dow Jones: +1.87% (YTD +9.1%)

- S&P 500: +3.53% (YTD +13.7%)

- Nasdaq: +5.61% (YTD +17.3%)

U.S. equities extended gains, with technology leading as optimism around AI and resilient corporate earnings offset slowing jobs growth. Payrolls averaged only 30k per month, pointing to labour market softness. Core PCE inflation slowed to 2.7% YoY, its lowest in two years, giving the Fed more room to ease policy.

Outlook:

Supportive earnings and imminent monetary easing are constructive, though stretched valuations and political risks around Fed independence temper the upside.

Europe: Modest Gains Amid Fiscal Risks

Equity Performance:

- Euro Stoxx 50: +3.23% (YTD +12.8%)

- FTSE 100: +1.78% (YTD +14.4%)

European equities gained, supported by industrials and banks, but persistent fiscal concerns in France and sticky UK inflation (CPI 3.7% YoY) limited momentum. Gilt yields remained high, underscoring the challenge for the Bank of England in balancing growth and inflation.

Outlook:

Dividends and resilient corporates remain supportive, but political and fiscal headwinds will constrain upside into Q4.

Japan: Strong Momentum, Rising Inflation Pressure

Equity Performance:

- Nikkei 225: +5.18% (YTD +12.6%)

Japan outperformed, lifted by solid Q2 GDP growth (+0.4% q/q), robust machinery orders, and healthy export demand. Inflation, however, stayed elevated at 3.5% core-core, driving 10-year JGB yields to 1.64%, the highest since 2008.

Outlook:

Exports and corporate investment underpin growth, but persistent inflation and potential BoJ tightening are risks to watch.

China: Mixed Signals: Mainland muted, offshore rebound

Equity Performance:

- Shanghai Composite: +0.64% (YTD +15.8%)

- Hang Seng: +7.09% (YTD +33.9%)

China led the advance, with offshore Chinese equities surging as the US–China trade truce was extended and AI optimism accelerated. Policy support – RRR cuts, industrial subsidies and new infrastructure – lifted sentiment and industrial output firmed; onshore gains were more muted as retail and property remained soft.

Outlook:

Policy support should cushion activity and aid select technology and industrial beneficiaries, but a durable re-rating likely requires a clearer turn in household demand and property stabilization. Expect uneven, policy-dependent progress into Q4.

South Africa: Resources Lead, Financials and Property Weaken

Equity Performance:

- JSE All Share: +5.99% (YTD +28.4%)

- Resource 10: +27.40% (YTD +116.6%)

- Industrial 25: +1.34% (YTD +19.7%)

- Financial 15: −2.75% (YTD +2.8%)

- Listed Property: −0.96% (YTD +12.3%)

The JSE gained nearly 6% in September, but performance was highly uneven. Resources soared over 27% as precious metals surged, while industrials posted only modest gains and financials and property declined.

The rand strengthened +2.2% vs USD to 17.27, supported by dollar weakness and commodity inflows. Local bonds rallied, with the 10-year yield falling to 9.16% (−45 bps). Inflation edged higher to 3.7% YoY, still well within target.

Outlook:

Resources remain the key driver, but domestic growth and fiscal risks highlight the importance of sectoral diversification.

Commodities and Currencies: Gold at Records, Oil Stabilises

Gold surged +12% in September to ~$3,858/oz, a new record, supported by safe-haven flows, central bank buying, and broad dollar weakness. Oil prices steadied, with Brent crude up +2% to ~$67/bbl, as OPEC+ supply discipline offset softer demand indicators.

Currencies reflected the weaker dollar backdrop. The rand gained +2.2% to 17.27 vs USD, while sterling (1.34) and the euro (20.26 vs ZAR) also advanced. Emerging-market peers such as the Brazilian real and Mexican peso strengthened, benefitting from improved global risk sentiment.

Fixed Income: Global Rally with Local Outperformance

Global bond markets rallied in September as investors priced in policy easing. The U.S. 10-year yield eased to 4.15% (−8 bps), supported by softer data. Gilts (4.70%) and bunds (2.71%) also edged lower, reflecting slowing growth despite sticky inflation.

Japan diverged, with yields rising to 1.64% (+3 bps) on persistent inflation. South African bonds outperformed strongly, with the 10-year yield falling 45 bps to 9.16%. Foreign inflows, rand strength, and attractive real yields supported performance, making local bonds a standout within EM debt.

Final Thoughts: Constructive but Cautious into Q4

September capped a strong Q3, with equities, credit, and EM currencies all advancing. Policy easing expectations and commodity-driven earnings have been tailwinds. However, risks remain elevated: valuations are stretched, fiscal and political uncertainty persists, and global trade disputes could resurface quickly.

What this means for portfolios:

- Maintain broad diversification across geographies, asset classes, and sectors.

- Blend growth with defensives to balance stretched valuations.

- Retain alternatives as hedges against political, policy, and trade-related shocks.

- As Q4 begins, investors should remain disciplined, avoid reacting to short-term headlines, and stay focused on long-term objectives.

_10072025-1")