As we bid farewell to June and conclude the second quarter of 2023, it’s essential to reflect on the plethora of news and data that has shaped the past three months. From inflation and interest rates to GDP figures, US debt ceiling negotiations, and attempted coups in Russia, the market has experienced a whirlwind of developments. In this review, we will deviate slightly from our usual Weekly Review format to highlight key events of the quarter and unpack market performance over the year thus far.

Let’s first begin with a look at what transpired over the past week:

- In the US, constructive inflation and growth data surprised to the upside, assisting major equity markets to round out a solid quarter. The S&P 500 index recorded its best weekly gain since March. The tech-heavy Nasdaq Composite ended the week with a six-month gain of nearly 32%, its best start to a year since 1983.

- Eurozone annual inflation slowed for the third consecutive month in June, down to 5.5% from 6.1% in May, below economists’ forecasts of 5.6%. Core inflation – which excludes energy, food, alcohol & tobacco prices – ticked slightly higher to 5.4% from 5.3%.

- Bank of England (BoE) Governor Andrew Bailey suggested that UK interest rates are likely to remain higher for longer. Borrowing costs could rise from 5% now to 6.5% by the end of the year, before falling in 2024.

- In China, official manufacturing PMI (Purchasing Managers’ Index) picked up to 49.0 in June, in line with expectations, up from 48.8 registered in May. A PMI reading less than 50 indicates a contraction in activity. Stocks ended mixed, as this weak economic data weighed on investor sentiment.

QUARTERLY SUMMARY

April 2023:

Finland made an impactful decision, after seven decades of military non-alignment and neutrality, Finland officially joined the North Atlantic Treaty Organization (NATO) as its 31st member. This move not only doubled NATO’s border with Russia but also bolstered its eastern flank, which holds great importance as the conflict in Ukraine persists.

Turning to China, the first-quarter GDP growth surpassed expectations, rising by 4.5% quarter-on-quarter, outperforming the estimated 4%. Despite some data falling below estimates, the overall surge in GDP growth signifies a return to normalcy and positions China on track to achieve its growth target of 5% or higher for the year.

India overtook China as the world’s most populous country, according to the United Nations. Furthermore, India’s population is projected to continue growing for several decades, while China’s population is expected to decline.

May 2023:

Moving on to the UK housing market in May, there were signs of stabilization as mortgage approvals for home purchases increased for the second consecutive month. The number of approved mortgages rose sharply to 52,011, the highest figure since October 2022.

Ukrainian President Volodymyr Zelenskyy travelled to Japan for diplomatic talks with the leaders of the Group of Seven (G-7) nations. The G-7 decided against implementing a near-outright ban on exports to Russia but opted to expand existing sanctions and restrictions on key Russian sectors such as manufacturing, construction, transportation, and business services.

In South Africa, Eskom’s warning about potential power cuts of up to 8,000 megawatts added further pressure to the country’s already fragile economic growth prospects. Loadshedding, is estimated to reduce economic growth by as much as two percentage points. South Africa’s unemployment rate in the first quarter of 2023 stood at 32.9%, ranking among the highest globally.

The European Commission raised its forecasts for Eurozone economic growth in 2023 and 2024, while anticipating persistently high inflation. The latest projection predicts a GDP expansion of 1.1% this year and 1.6% in 2024, up from the previous estimates of 0.9% and 1.5% respectively.

In a significant development, President Joe Biden and House Speaker Kevin McCarthy reached a tentative agreement to raise the US debt ceiling, ending months of stalemate. Republicans seeking spending cuts in areas such as education and social programs in exchange for raising the debt limit, which currently stands at $31.4 trillion.

June 2023:

The foreign ministers of Brazil, Russia, India, China, and South Africa (BRICS) gathered in Cape Town. The BRICS nations have requested guidance from their dedicated bank regarding the potential implementation of a shared currency, aiming to shield member countries from the impact of sanctions similar to those imposed on Russia. Additionally, South Africa saw a significant narrowing of its current account deficit from 2.3% to 1.0% of GDP in Q1 2023, defying consensus forecasts of a widening deficit.

The World Bank has revised its global GDP forecast for 2023, increasing it from the earlier projection of 1.7% to 2.1%. While this adjustment indicates an improvement, it also suggests a significant deceleration compared to the 3.1% growth rate observed in 2022. Additionally, the World Bank has lowered its growth outlook for 2024 from 2.7% to 2.4%.

US inflation witnessed a notable decrease, reaching its lowest annual level in over two years, as reported by the Labor Department. The consumer price index rose by only 0.1% during the month, resulting in a decline in the annual rate from 4.9% in April to 4% in May. However, core inflation, which excludes volatile food and energy prices, increased by 0.4% for the month and remained 5.3% higher than the previous year.

The Federal Reserve decided to maintain interest rates at their current levels, choosing to assess the impacts of the previous 10 rate hikes. The positive inflation data helped investors absorb the somewhat hawkish outlook from Fed policymakers.

Shifting our focus to the Bank of England, it implemented a surprising 50 basis point interest rate hike, pushing the lending rate to 5%. The rate hike was prompted by persistently high inflation, with core inflation reaching its highest level since 1992.

Lastly, Russian President Vladimir Putin firmly pledged to deliver consequences to those responsible for the “armed uprising” following an apparent insurrection led by the head of the Wagner private military group. The insurrection involved the takeover of military installations in Rostov-on-Don and Voronezh and included a warning of troops potentially advancing toward Moscow, posing a threat to Putin’s 24-year rule.

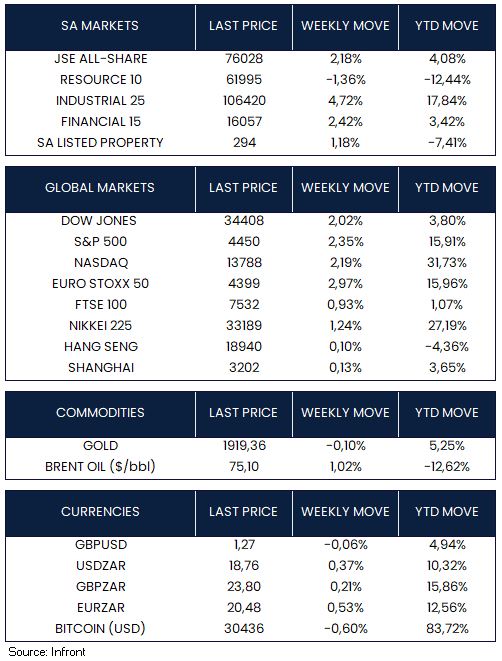

US stocks ended the week higher, with the S&P 500 up 2.35% (15.91% YTD), the Dow Jones Industrial Average up 2.02% (3.80% YTD), and the tech heavy Nasdaq Composite rising 2.19% (31.73% YTD). On share specific news, Apple closed trading on Friday with a market cap above $3 trillion, a first for any publicly traded company.

The positive trend carried through to Europe and the UK. Euro Stoxx 50 ended the weak higher 2.97% (15.96% YTD), the FTSE 100 closed the week in positive territory up 0.93% (1.07% YTD). Japan’s Nikkei 225 index gained 1.24% this week, continuing its positive trend for the year (27.19% YTD). Chinese equities closed the week marginally higher the Hang Seng Composite up 0.10% (-4.36% YTD) and Shanghai Composite up 0.13% (3.65% YTD).

Market Moves of the Week:

Global risk on factors filtered through to the local market this week, the JSE ALSI posted strong performance for the week 2.18% (4.08% YTD), both industrials and financials contributed to the positive return, up 4.72% and 2.42% respectively. Further pressure in the Resource sector detracted from the ALSI performance, -1.36% for the week and down 12.44% YTD.

The Rand was slightly weaker against the dollar, depreciating 0.37% this week. The currency was trading at R18.76/$ by Friday close. The SA listed property sector had a positive week, up 1.18%, however the sector is still in the red on a YTD basis, down 7.41%.

Chart of the Week:

The disparity in market capitalisation between the United States (US) and emerging markets (EM) has now exceeded a staggering $18 trillion. Forecasts suggest that by the end of the current decade, EM stock market capitalisation will outpace that of the US, driven by increasing incomes and enhanced investor access to public markets. Currently, EM is significantly underrepresented, constituting only around 27% of the total global market capitalisation, despite accounting for approximately 45% of the global Gross Domestic Product (GDP) when measured in US dollars. The projected ascent of EM from 27% to 35% will serve as a strong tailwind, propelling these markets towards greater prominence and influence.

Source: Bloomberg & Goldman Sachs Group Inc.