The U.S. economy exceeded expectations in the final quarter of 2023, with a revised annual growth rate of 3.4%, up from the previous estimate of 3.2%. Strong personal consumption and robust corporate profits were key drivers. Overall, U.S. real GDP for 2023 increased by 2.5%. Nowcast models from the Federal Reserve (the Fed) Banks of New York and Atlanta predict a growth rate of around 2% in the first quarter of 2024.

The Fed’s preferred inflation measure, the core personal consumption expenditures price index (PCE), which excludes food and energy, increased 2.8% y/y in February, matching estimates. The Fed targets 2% annual inflation; core PCE inflation hasn’t been below that level in three years. Jerome Powell remarked that the PCE report released on Friday, along with other recent data, indicated that progress towards the 2 percent target was occasionally bumpy. The latest projections from the Fed indicated that officials still anticipated reducing rates by 0.75 percentage points this year, down from their 23-year high of 5.25-5.5%. In other U.S. news, on Tuesday, ratings agency S&P Global downgraded five regional U.S. banks due to their commercial real estate exposures. This action is expected to revive investor concerns regarding the sector’s health.

European Central Bank (ECB) board member Piero Cipollone stated on Wednesday that the ECB is growing more confident of inflation returning to its 2% target by mid-2025 as wage growth eases, bolstering the argument for reduced interest rates. He indicated that the ECB has hinted at a potential rate cut in June, contingent on positive wage developments. Investors are anticipating an ECB rate cut in June, although opinions are divided on whether two or three additional moves will follow before the year concludes.

This week, China’s President, Xi Jinping, held discussions with U.S. business leaders during the China Development Forum, an annual conference in Beijing. In recent months, China has aimed to create a more hospitable environment for international businesses, particularly after foreign direct investment reached its lowest levels in decades last year. Official statistics released Wednesday indicate that China’s economy is displaying signs of stabilization, with industrial profits increasing by 10.2% for the January to February period compared to the previous year. However, this growth was partly attributed to a low base in 2023.

Despite the Bank of Japan’s (BoJ) recent decision to discontinue negative interest rates, the yen depreciated to a 34-year low of 151.97 against the U.S. dollar on Wednesday. Japanese authorities voiced their objection to these developments, describing them as disorderly. The historic weakness in the yen has benefited many of Japan’s large-cap exporters, as they derive a significant share of their earnings from overseas. Market expectations are converging on the likelihood of two more BoJ interest rate hikes within a year.

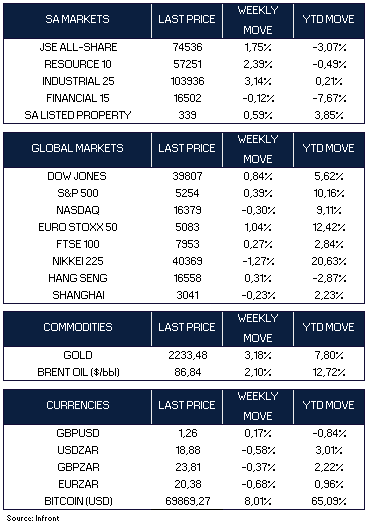

On the market front, most of the major U.S. benchmarks ended the week higher, to end a quarter of strong gains. The S&P 500 index rose by +0.39%, recording new closing and intraday highs to end the week. The Dow Jones also ended the week higher, up +0.84%, while the Nasdaq Composite slipped -0.30%. The yield on the U.S. 10-year benchmark note remained largely unchanged at 4.22%.

In Europe, the Euro Stoxx 50 index gained +1.04%, despite confirmation of a significant slowdown in some major economies while the UK’s FTSE 100 climbed +0.27%. Chinese stocks declined slightly (Shanghai Composite Index down -0.23%), whereas Hong Kong shares (Hang Seng index) rose +0.31%. Japan’s stock market dipped, with the Nikkei 225 losing -1.27%. Oil prices (Brent) gained +2.10% while Gold rose by +3.18%.

Market Moves of the Week

The South African Reserve Bank’s (SARB) Monetary Policy Committee (MPC) kept its repo rate unchanged at 8.25% in a unanimous decision (as expected) on Wednesday. While its forecasts stayed largely consistent, the MPC’s commentary on inflation adopted a more hawkish tone. The Committee cited mounting upside risks to the inflation outlook, stemming mainly from the threat posed by adverse weather conditions to domestic food production and its likely impact on food prices. Meanwhile, the MPC pointed out that interest rate differentials, terms of trade, and election risk have exerted downward pressure on the Rand, which it perceives as being “undervalued”.

On Tuesday, Statistics South Africa (Stats SA) reported that formal employment in the country decreased by 194,000 jobs, or -1.8% q/q, for the fourth quarter of 2023. This brought the level of employment to 10.7 million. Several industries witnessed declines in full-time employment, with the construction sector, manufacturing industry and community services industry experiencing the most significant decline. Conversely, the trade industry reported an increase of 31,000 jobs.

Private sector credit extension (PSCE) growth drifted sideways in February, as consensus expected (3.3% y/y in February from 3.2% y/y in January). Credit trends generally remain quite weak in SA and well below inflation. Persistent weakness in this data has a dovish read-through for monetary policy, even though it hasn’t been a key determinant of the SARB’s interest rate decisions in recent months.

The JSE gained +1.75% over the shortened trading week, with Industrials (+3.14%) leading the advance. Resources (+2.39%) maintained their recent bullish momentum on the back of rising commodity prices. The local currency strengthened against the U.S. dollar over the week, falling to R18.88/$ from last week’s R18.99/$ level.

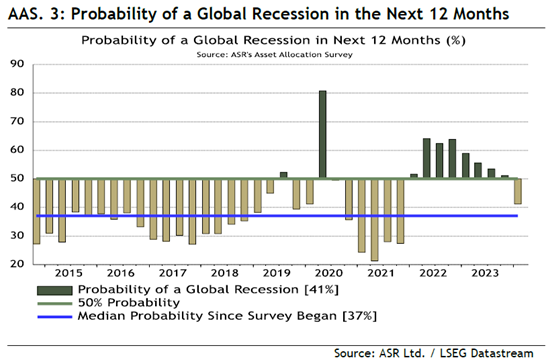

Chart of the Week

The latest Asset Allocators survey by Absolute Strategy Research, which polls 225 managers overseeing $8 trillion, indicates a notable decrease in the likelihood of a recession within the next 12 months. This is the first time in two years that the probability of a recession, as assessed by these allocators, has dropped below 50%. Source: Bloomberg.