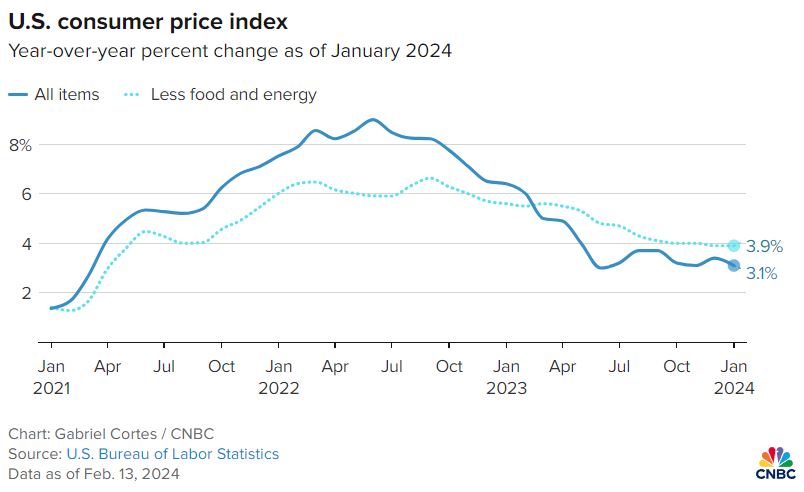

U.S. consumer prices rose more than expected in January, amid stubbornly high shelter prices. The increase in prices reported by the Labor Department on Tuesday was the largest in four months, the report showed that inflation last month remained high with consumer prices rising by 3.1% in January from a year ago. Although that is cooler than in December, economists surveyed by Dow Jones had been looking for a monthly increase of 0.2% and an annual gain of 2.9%.

Excluding volatile food and energy prices, core CPI accelerated 0.4% in January and was up 3.9% from a year ago, unchanged from December. The forecast had been for 0.3% and 3.7%, respectively.

Shelter prices, which comprise about one-third of the CPI weighting, accounted for much of the rise. The index for that category climbed 0.6% on the month, contributing more than two-thirds of the headline increase. Fed officials expect inflation to recede back to their 2% annual target in large part because they think shelter prices will decelerate through the year. According to the CME FedWatch Tool, the futures market ended the week pricing in only a 10% chance of a rate cut in March compared with a 53% chance a month earlier.

The hotter than expected inflation report was followed on Thursday by a softer than expected retail sales report. The Commerce Department reported that retail sales had fallen 0.8% in January (forecast was for a 0.3% decline). While many economists pointed to seasonal factors, the prior two months’ readings were also revised lower.

In local currency terms, the pan-European STOXX Europe 50 Index ended the week 1.06% higher as signs of cooling inflation in the eurozone and a better outlook for interest rate cuts improved investor sentiment.

During the week, the European Commission downgraded its growth forecast to 0.8%, down from its previous forecast of a 1.2% expansion. The commission sees eurozone inflation falling to 2.7% in 2024 from 5.7% in 2023, a steeper drop than its earlier 3.2% forecast.

In the UK, initial figures from the office for national statistics showed on Thursday that the UK economy slipped into a technical recession in the final quarter of last year. A preliminary estimate of gross domestic product (GDP) showed a greater-than-expected contraction of 0.3% in the three months through December. The economy shrank 0.1% between July and September. Two straight quarters of negative growth is widely considered a technical recession.

Japan’s stock markets rose over the week, with the Nikkei 225 Index gaining 4.3% driven by further Yen weakness and positive corporate earnings releases. The Japanese economy contracted 0.4% quarter on quarter over the final three months of last year, a worse-than-expected slump, which similarly to the UK marked an entry into a technical recession. The country’s economy is now the world’s fourth largest, slipping behind Germany in gross domestic product terms.

Financial markets in mainland China were closed for the weeklong Lunar New Year and reopen on Monday.

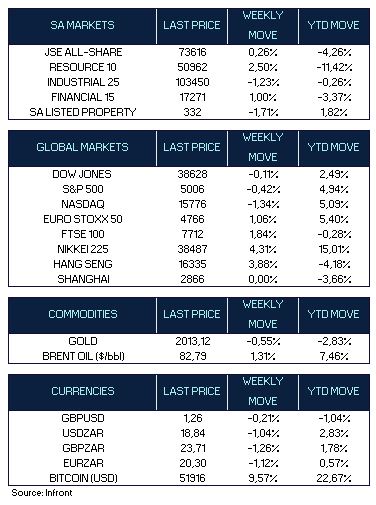

Gold headed for a second consecutive weekly fall on Friday, ending the week at $2,013/oz, down 0.55% for the week, while oil prices ended the week higher as geopolitical tensions in the Middle East more than offset a forecast from the International Energy Agency for slowing demand. Brent crude ending the week 1,31% higher at $82.79 a barrel.

Market Moves of the Week

In South Africa, December retail sales published by Stats SA on Wednesday surprised to the upside, gaining 2.7% from a year earlier. The print was higher than market expectations, but economists warned the sector is still expected to detract from overall GDP in the fourth quarter due to muted consumer spending.

South Africa’s Minister of Finance, Enoch Godongwana will present the 2024 Budget speech this week on 21 February, outlining government’s financial and economic agenda for the year ahead. The 2024 Budget is expected to focus on continued fiscal discipline whilst balancing big-risk expenditure line items such as the public sector wage bill, support for Transnet and other SOE’s as well as the increasing fiscal burden of social grants.

The JSE all share ended the week marginally positive (0.26%) – with major indices mixed. The resource (2.5%) and financial (1%) sectors ended the week stronger while the industrial and listed property sector lost 1.23% and 1,71% respectively. The rand strengthened over the week as the dollar weakened, to end the week over 1% stronger at R18.84/$.

Chart of the Week

The consumer price index rose more than expected in January, increasing 0.3% for the month. On a 12-month basis, that came out to 3.1%, down from 3.4% in December. Shelter prices accounted for much of the rise, climbing 0.6% on the month, contributing more than two-thirds of the headline increase. Core CPI (which excludes volatile food & energy prices) accelerated 0.4% in January and was up 3.9% from a year ago, unchanged from December.