The Federal Reserve (the Fed), the European Central Bank (ECB) and the Bank of Japan (BoJ) all made significant announcements this week. The Fed delivered another interest rate hike this week, as expected, while Chair Jerome Powell indicated that there might be additional hikes in the future, depending on the incoming data, which has recently shown a robust U.S. economy. The unanimous decision to raise rates by a quarter percentage point has pushed the target range for the Fed’s benchmark federal funds rate to 5.25% – 5.5%, the highest level in 22 years. The Fed revised its evaluation of U.S. growth, upgrading it from “modest” to “moderate,” whilst eliminating its recession forecast. Powell also stated that rate cuts are improbable in the upcoming year and noted that inflation is not expected to reach the target until 2025.

On Thursday, the ECB increased the key interest rate in the eurozone by 0.25 percentage points, bringing its main rate to 3.75%, a record-equalling high. ECB President, Christine Lagarde, said that the bank might hike or hold rates steady in September. “The Governing Council will continue to follow a data-dependent approach to determining the appropriate level and duration of restriction,” the ECB said in its statement. Earlier this week, business activity data from the eurozone indicated declines in the economies of its major players, Germany and France. These figures have heightened concerns that the euro area might face the risk of slipping back into recession in the current year.

In a surprising move, the BoJ made adjustments to its monetary policy, revealing plans to enhance flexibility regarding its yield curve control (YCC) target, which is designed to keep Japanese government bond yields in a narrow corridor. The bank announced that the previous 0.5% cap on 10-year Japanese Government Bond (JGB) yields will now serve as a reference level. Going forward, the bank will intervene in a flexible manner to restrain yields, setting a new cap at 1%. The move is expected to enhance the sustainability of monetary easing under the current framework. Additionally, as anticipated, the BoJ raised its forecast for consumer price inflation in fiscal 2023.

On the economic data front, the preliminary U.S. GDP data revealed a growth of 2.4% in the second quarter, driven by robust consumer spending and non-residential investment – raising hopes of a possible “soft landing”. This rate of growth topped the 2% pace recorded in the first quarter and strongly beat consensus estimates of a 1.8% expansion. Likewise, U.S. consumer confidence increased to a two-year high in July, supporting the economy’s prospects in the near term. In inflation-related news, the core personal consumption expenditures price index, the Fed’s preferred measure of inflation, rose 4.1% y/y, the lowest annual increase since September 2021 and marked a decrease from the 4.6% level in May.

Based on data from FactSet Research, as of Q2 2023, slightly over half of the companies in the S&P 500 Index have reported their earnings. The blended earnings per share, which incorporates both reported data and estimates for yet-to-report companies, indicate a 7.5% decline compared to the same quarter the previous year. The energy and materials sectors experienced the most significant drops, while the consumer discretionary sector exhibited the strongest growth. Additionally, sales remained flat year over year.

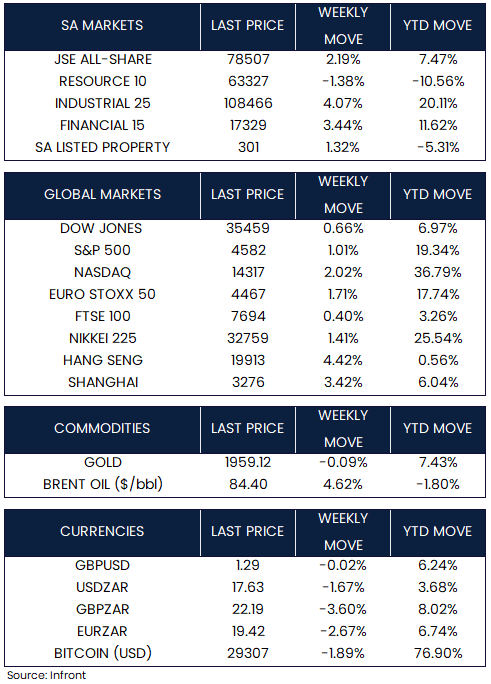

On the market front, global indices ended the week in the green. The S&P 500 Index climbed +1.01%, while the Dow Jones rose by +0.66%, notching its 13th consecutive daily gain on Wednesday, which marked its longest winning streak since 1987. The technology-heavy Nasdaq Composite outperformed and ended the week up +2.02%. Shares in Europe rose +1.71% (Euro Stoxx 50) over the week while the FTSE 100 managed a 0.40% gain.

Chinese equities rallied after Beijing signalled it would provide more stimulus to support the economy. The Shanghai and Hang Seng index ended the week up +3.42% and +4.42% respectively. In Japan, the Nikkei 225 gained +1.41%. Gold dipped -0.09% while Brent Oil rose +4.62% over the week.

Market Moves of the Week:

South Africa’s June Producer Price Inflation (PPI) was released this week. The index decelerated to 4.8% y/y, down from 7.3% in May – the biggest drop in more than a decade and the lowest level since February 2021. The main contributor to the downward trend was the category of ‘coke, petroleum, chemicals, rubber, and plastic products’, with the ‘food products’ category following closely behind. The move added momentum to the argument that rate hikes have achieved their objectives.

The International Monetary Fund, on Tuesday, stated that South African output would experience a +0.3% increase in 2023, primarily due to the resilience shown by its services sector during the first quarter, despite the ongoing electricity crisis. This updated forecast represents an increase from the +0.1% growth expectation stated in the IMF’s World Economic Outlook report in April 2023.

According to data from JSE Ltd., foreign investors purchased 14.1 billion rand ($784 million) of the country’s debt last Friday. This represents the largest net inflow recorded since the exchange operator started publishing such data in 2019.

Russian President Vladimir Putin announced that his nation and the African leaders participating in a summit in St. Petersburg have reached a consensus to advocate for a multipolar world order and combat “neocolonialism.” During the two-day summit, Putin offered debt write-offs and grain as incentives to attract allies. He emphasized that Russia’s interest in Africa has been consistently increasing. The meeting was seen as a test of Moscow’s support in Africa, where Russia retains backing despite international isolation sparked by its war in Ukraine. South African President Cyril Ramaphosa said African leaders were looking forward to engaging further with Putin later Friday on their peace proposal.

The JSE (+2.19%) rose over the week, in line with international peers. Resources (-1.38%) were the outlier, as all other major sectors ended in the green. The rand appreciated against the U.S. dollar over the week, strengthening to R17.63/$ from last week’s R17.93/$ level.

Chart of the Week:

The Dollar has been overvalued for almost a decade. Portfolio flows chasing ‘U.S. exceptionalism’ and escaping more challenging risk-adjusted returns abroad (over the past year) provide structural support to the Dollar’s high valuation. However, there is a strong consensus that the Dollar should fall over the next year as the Fed most likely ends its rate hiking cycle.

Source: Infront, Goldman Sachs