The past week witnessed a varied performance in the major U.S. stock markets. Investors grappled with the implications of subdued inflation data against concerns stemming from the recent uptick in lon…

Continue readingThe past week witnessed a varied performance in the major U.S. stock markets. Investors grappled with the implications of subdued inflation data against concerns stemming from the recent uptick in lon…

Continue reading

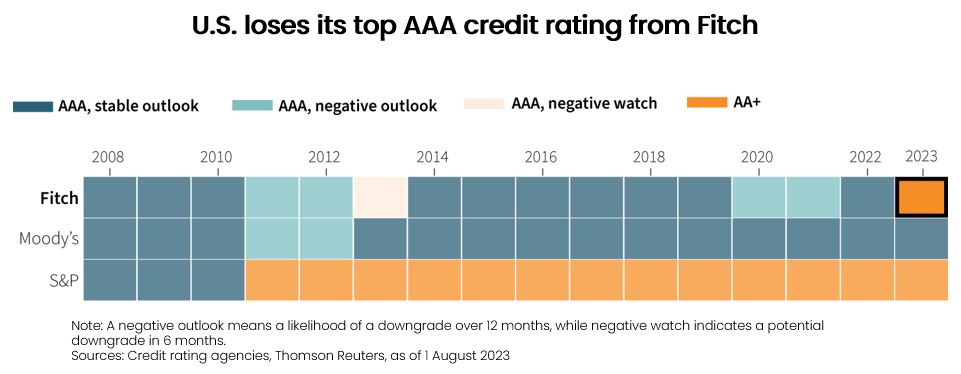

Global equity markets had a tough start to August, as Fitch Ratings unexpectedly downgraded the U.S.’s credit rating from AAA to AA+. This marked the second credit downgrade in U.S. history, raising concerns about the country’s fiscal outlook and highlighting ongoing fiscal challenges worldwide. While the impact on financial markets may be limited, it remains an important development.

U.S. employment data was in the spotlight this week, with data showing that 187,000 jobs were added in July, similar to June’s figures. This suggests that the pace of job growth has slowed compared to earlier months, where an average of 287,000 jobs were added per month in the first half of the year. The unemployment rate declined slightly to 3.5%, and wages grew by 4.4% year-on-year, indicating that the U.S. labour market is cooling just enough, adding more support to a possible soft landing for the world’s largest economy.

Other U.S. economic indicators were mixed in July, with some meeting expectations and others falling short. The eurozone, on the other hand, saw a surprising 0.3% growth in Q2, exceeding expectations. Inflation in the euro area slowed to 5.3% in July but remained well above the European Central Bank’s target of 2%.

The Bank of England (BoE) raised its key interest rate to 5.25%, the highest in 15 years, with plans to keep rates high to combat inflation. The BoE’s economic growth estimates for this year and the next remained at 0.5%. However, the UK housing market faces challenges with falling house prices and the first quarterly decline in net mortgage lending since 1987.

China experienced a decline in its manufacturing PMI, signalling contraction, while home sales faced setbacks. However, the services PMI showed growth, highlighting resilience in the services sector. In Japan, the unemployment rate improved, together with services PMI, but the manufacturing PMI fell below expectations.

In other news, heads of state from BRICS nations are set to discuss the enlargement of the group. Twenty-two nations have asked formally to become full-time members of the group, and more than 20 others have submitted informal requests. China seeks rapid expansion, while India and Brazil have concerns about the rules and potential repercussions on international relations.

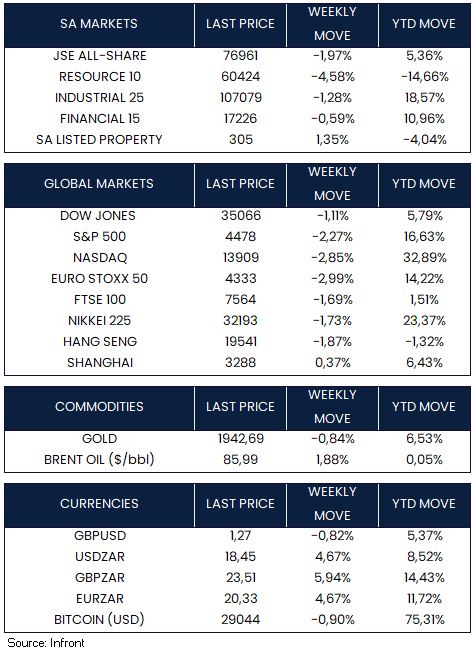

Global equity markets concluded the week with losses. In the U.S., the Dow Jones (-1.11%), S&P 500 (-2.27%), and Nasdaq (-2.85%) all closed the week in the red. Similarly, European and Asian markets, including the Euro Stoxx 50 (-2.99%), FTSE 100 (-1.69%), Nikkei 225 (-1.73%), and Hang Seng (-1.87%) indices, experienced declines, with the Shanghai Composite Index (+0.37%) being the exception.

South Africa’s trade balance saw a sharp decline in June, shifting from a surplus of R9.58bn in the previous month to a deficit of R3.54bn. This was mainly driven by a significant drop in exports, contributing to a projected widening of the overall current account deficit from 1.0% of GDP in Q1 to 2.7% of GDP in Q2.

New vehicle sales saw a year-on-year improvement of approximately 1% in July, with 43,389 units sold compared to 42,822 units in July 2022. The overall trend for the past three months showed a positive growth of 8% year-on-year in total new vehicle sales, driven by strong performance in the light and heavy commercial segments, which grew by 42% and 23% respectively.

Eskom reported a substantial increase in distributed-generation solar PV capacity, with 1.82 GW added in the first six months of the year. Installed solar rooftop PV capacity rose from 983 MW in March to 4,411.5 MW in June. However, there are concerns that the reported figures might be overstated.

The JSE All-Share Index (-1.97%) was negative this week. Weaker performances came from all three of the major indices including the resource (-4.58%), industrial (-1.28%) and financial (-0.59%) sectors. By Friday close, the rand was trading at R18.45 to the U.S. Dollar, depreciating by -4.67% for the week.

Fitch downgraded the United States’ credit rating from AAA to AA+ on Tuesday, triggering strong reactions from the White House and surprising investors. This decision came despite resolving the debt ceiling crisis two months earlier. Fitch cited concerns about the country’s financial outlook over the next three years and the recurring last-minute debt ceiling negotiations that threaten the government’s ability to meet its financial commitments. The chart shows that Fitch downgraded the U.S.’s long-term foreign currency rating to AA+ in 2023, following a similar move by S&P in 2011.

Source: Thomson Reuters.

Global equity markets had a tough start to August, as Fitch Ratings unexpectedly downgraded the U.S.’s credit rating from AAA to AA+. This marked the second credit downgrade in U.S. history, raising concerns about the country’s fiscal outlook and highlighting ongoing fiscal challenges worldwide. While the impact on financial markets may be limited, it remains an important development.

U.S. employment data was in the spotlight this week, with data showing that 187,000 jobs were added in July, similar to June’s figures. This suggests that the pace of job growth has slowed compared to earlier months, where an average of 287,000 jobs were added per month in the first half of the year. The unemployment rate declined slightly to 3.5%, and wages grew by 4.4% year-on-year, indicating that the U.S. labour market is cooling just enough, adding more support to a possible soft landing for the world’s largest economy.

Other U.S. economic indicators were mixed in July, with some meeting expectations and others falling short. The eurozone, on the other hand, saw a surprising 0.3% growth in Q2, exceeding expectations. Inflation in the euro area slowed to 5.3% in July but remained well above the European Central Bank’s target of 2%.

The Bank of England (BoE) raised its key interest rate to 5.25%, the highest in 15 years, with plans to keep rates high to combat inflation. The BoE’s economic growth estimates for this year and the next remained at 0.5%. However, the UK housing market faces challenges with falling house prices and the first quarterly decline in net mortgage lending since 1987.

China experienced a decline in its manufacturing PMI, signalling contraction, while home sales faced setbacks. However, the services PMI showed growth, highlighting resilience in the services sector. In Japan, the unemployment rate improved, together with services PMI, but the manufacturing PMI fell below expectations.

In other news, heads of state from BRICS nations are set to discuss the enlargement of the group. Twenty-two nations have asked formally to become full-time members of the group, and more than 20 others have submitted informal requests. China seeks rapid expansion, while India and Brazil have concerns about the rules and potential repercussions on international relations.

Global equity markets concluded the week with losses. In the U.S., the Dow Jones (-1.11%), S&P 500 (-2.27%), and Nasdaq (-2.85%) all closed the week in the red. Similarly, European and Asian markets, including the Euro Stoxx 50 (-2.99%), FTSE 100 (-1.69%), Nikkei 225 (-1.73%), and Hang Seng (-1.87%) indices, experienced declines, with the Shanghai Composite Index (+0.37%) being the exception.

South Africa’s trade balance saw a sharp decline in June, shifting from a surplus of R9.58bn in the previous month to a deficit of R3.54bn. This was mainly driven by a significant drop in exports, contributing to a projected widening of the overall current account deficit from 1.0% of GDP in Q1 to 2.7% of GDP in Q2.

New vehicle sales saw a year-on-year improvement of approximately 1% in July, with 43,389 units sold compared to 42,822 units in July 2022. The overall trend for the past three months showed a positive growth of 8% year-on-year in total new vehicle sales, driven by strong performance in the light and heavy commercial segments, which grew by 42% and 23% respectively.

Eskom reported a substantial increase in distributed-generation solar PV capacity, with 1.82 GW added in the first six months of the year. Installed solar rooftop PV capacity rose from 983 MW in March to 4,411.5 MW in June. However, there are concerns that the reported figures might be overstated.

The JSE All-Share Index (-1.97%) was negative this week. Weaker performances came from all three of the major indices including the resource (-4.58%), industrial (-1.28%) and financial (-0.59%) sectors. By Friday close, the rand was trading at R18.45 to the U.S. Dollar, depreciating by -4.67% for the week.

Fitch downgraded the United States’ credit rating from AAA to AA+ on Tuesday, triggering strong reactions from the White House and surprising investors. This decision came despite resolving the debt ceiling crisis two months earlier. Fitch cited concerns about the country’s financial outlook over the next three years and the recurring last-minute debt ceiling negotiations that threaten the government’s ability to meet its financial commitments. The chart shows that Fitch downgraded the U.S.’s long-term foreign currency rating to AA+ in 2023, following a similar move by S&P in 2011.

Source: Thomson Reuters.

The Fed delivered another interest rate hike this week, as expected, while Chair Jerome Powell indicated that there might be additional hikes in the future, depending on the incoming data…

Continue reading

In June, spending at US retailers continued its positive growth trend for the third consecutive month, showcasing resilience among American consumers. According to the Commerce Department’s report on…

Continue reading

After more than 50 ministers and several Cabinet members stepped down, U.K Prime Minister Boris Johnson announced his intention to resign. This comes weeks after Johnson narrowly survived a no confide…

Continue reading

After a strong performance in the first half of 2023, markets experienced a slight setback in the first week of the third quarter. The catalyst behind this week’s pullback was the release of the Fed’s…

Continue reading

As we bid farewell to June and conclude the second quarter of 2023, it’s essential to reflect on the plethora of news and data that has shaped the past three months. From inflation and interest rates…

Continue reading

On Thursday, the Bank of England, implemented a 50 basis point interest rate hike (pushing the lending rate to 5%), surprising markets that had priced in a 60% chance of a 25 bps hike. Following the decision, markets saw a nearly 50% chance that Bank Rate would peak at 6.25% by the end of this year. The move comes after U.K’s May inflation figure was published on Wednesday, which showed that inflation in the region remains stubbornly high, with core inflation rising to its highest level since 1992. Headline inflation defied predictions, coming in at 8.7% y/y vs 8.4% expected, keeping in line with April’s figure. Core inflation jumped 7.1% y/y, up from 6.8% in April. In May, the central bank forecasted that inflation would drop to just over 5% by year end and be below its 2% target in early 2025.

Keeping with the inflation theme, U.S. Federal Reserve Chair Jerome Powell stated this week, while addressing the Senate Banking Committee, that more rate hikes may be needed this year. Powell additionally mentioned that policymakers feel “it will be appropriate to raise rates again this year, and perhaps twice,” if the economy performs about as expected. Decisions will be made on a meeting-by-meeting basis, Powell said, while noting that there is a long way to go to get inflation back down to its 2% goal.

The latest release of flash purchasing managers index’s (PMI) data on Friday indicates a stagnation in the eurozone economy. The composite S&P Global PMI registered at 50.3. The manufacturing index declined from 44.8 in May to 43.6, while the services measure experienced a significant monthly deterioration, dropping from 55.1 to 52.4, which is an unusually substantial decrease.

On Saturday, Russian President Vladimir Putin made a firm commitment to mete out consequences to those responsible for an “armed uprising” following the apparent insurrection led by the head of the Wagner private military group – which threatened to end Putin’s 24-year rule. The insurrection involved taking control of military installations in two Russian cities, namely Rostov-on-Don and Voronezh, and included a warning that the troops could advance towards Moscow. In a sudden change of direction, Yevgeny Prigozhin, the leader of Wagner, announced that he had halted the advance of his troops towards Moscow and issued orders for them to evacuate Rostov. As part of a negotiated agreement facilitated by Belarus, Prigozhin agreed to depart from Russia and relocate to Belarus. In a statement, Prigozhin said that he wanted to avoid the spilling of “Russian blood”.

This week, the yen continued to depreciate against other major currencies, crossing the 143 mark against the dollar, coinciding with Japan’s announcement of its highest core inflation rate since 1981, standing at 4.1%. While other central banks adopted a more hawkish stance, the Bank of Japan maintained its super loose monetary policy approach. If the yen experiences further decline, it may necessitate adjustments to the Bank of Japan’s yield curve control policy.

No major indicators were released in China during the week. However, mounting evidence that the country’s recovery is losing steam raised fresh concerns about the economic outlook. China’s People’s Bank of China was the lone major central bank to lower rates this week, cutting the important loan prime rate 0.1% to 4.2% in an effort to lower borrowing costs and boost confidence and consumption.

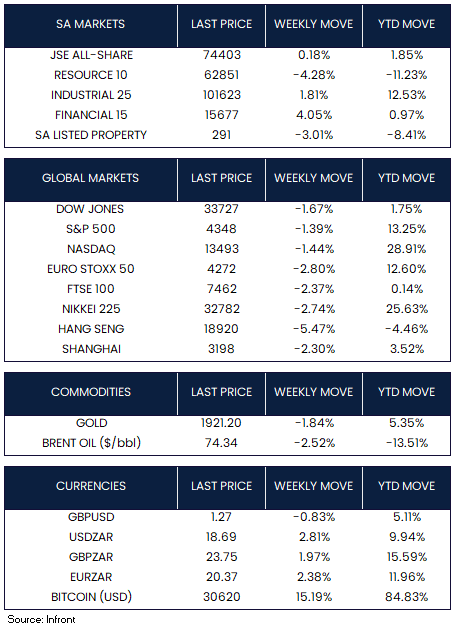

On the market front, global indices ended the week in the red. Growth stocks outperformed value shares, while large-caps fared better than small-caps. The S&P 500 Index fell -1.39%, while the Dow Jones slipped -1.67%. The technology-heavy Nasdaq Composite had a strong start to the week but ended the week down -1.44%. Shares in Europe (Euro Stoxx 50, -2.80%) and the UK (FTSE 100, -2.37%) fell over the week on worries that further interest rate increases might cause a recession in Britain and the eurozone.

Chinese shares (the Shanghai index) ended the week down -2.30%, while in Hong Kong, the benchmark Hang Seng Index declined -5.74%, its largest drop in three months. In Japan, the Nikkei 225 fell -2.74%. Gold dipped -1.84% while Brent Oil declined by -2.52% over the week.

Inflation in South Africa moderated and surprised to the downside in May, with headline inflation falling to 6.3% y/y (expectations: 6.5% y/y) from 6.8% y/y in April. Importantly, the inflationary impact of food and non-alcoholic beverages, which had been a major contributing factor in the recent months, was considerably lower than expected – coming in at 11.8% y/y vs April’s 13.9% y/y print. Last year’s high fuel price also fell out of the index’s base, improving the figure. The annual rate for fuel decreased to 3.5% from 5.0% in April. Core inflation also edged lower to 5.2% y/y, as expected. Moving forward, although inflation is starting to exhibit noticeable signs of decreasing, it remains above the South African Reserve Bank’s (SARB) target range of 3%-6%.

Given the downside surprises in inflation in the past two months, the strengthening of the rand and a decline in oil prices, the inflation outlook has improved. The market is gaining confidence that the SARB has completed its hiking cycle (staying on hold in July – the next Monetary Policy Committee meeting). However economists have not ruled out further hikes, saying this would depend on the course of load-shedding and the rand’s behaviour.

According to a statement from the South African presidency, Invest International, a company owned by the Netherlands finance ministry and state development bank FMO, has committed €300 million ($330 million) to establish a public infrastructure fund for investing in water and energy projects in South Africa. The funding will be provided through a combination of €200 million in loans and €100 million in grants.

Eskom is making progress in its efforts to restructure and operationalize its transmission company by November’s end. This is part of a comprehensive plan to improve the financial and operational performance of the financially struggling power utility. Eskom’s acting group CEO, Calib Cassim, informed members of parliament that two critical requirements remain for the successful spin-off of the transmission company. These include obtaining the transmission license from the National Energy Regulator of SA (Nersa) by the end of July and securing the consent of lenders, which is expected to be achieved by the end of August.

The JSE (+0.18%) managed a marginal gain over the week. Sectors were mixed with Resources selling off (-4.28%) and Financials rallying (+4.05%). The local currency weakened against the U.S. dollar over the week, rising to R18.69/$ from last week’s R18.18/$ level.

The persistence of the country’s cost-of-living crisis, with U.K. CPI the highest in the G7, will be a headache for the government. Prime Minister Rishi Sunak promised to halve inflation by the end of this year ahead of a general election in 2024.

Source: Reuters, CNBC

In May, the inflation rate witnessed a notable decrease, reaching its lowest annual level in over two years, as reported by the Labor Department. The consumer price index rose by only 0.1% during the month, resulting in a decline in the annual rate from 4.9% in April to 4% in May. While there has been some easing of price pressures, core inflation, which excludes volatile food and energy prices, increased by 0.4% for the month and remained 5.3% higher than the previous year.

At the wholesale level, US inflation has also experienced a decline, falling well below its pre-pandemic average. The Producer Price Index data released by the Bureau of Labor Statistics shows a modest 1.1% annual increase for the 12-month period ending in May, a sharp drop from the 2.3% growth recorded in April. This marks the lowest annual level since December 2020, with energy and food prices playing a significant role in the decline. On a monthly basis, prices saw a 0.3% decrease, reflecting the fourth decline in six months.

Despite these fluctuations, US retail sales demonstrated resilience and growth in May, defying expectations of a decline. The Commerce Department reported a 0.3% increase in retail sales across various outlets, including physical stores, online platforms, and restaurants, compared to April. This positive trend underscores the vital role of consumer spending in fuelling the economy. While gasoline stations and miscellaneous stores experienced a decrease in sales, spending grew in other categories. Excluding gasoline station sales, retail spending showed a stronger increase of 0.6%, with building materials and gardening items experiencing the highest surge of 2.2% in May. Overall, retail sales rose by 1.6% compared to the previous year.

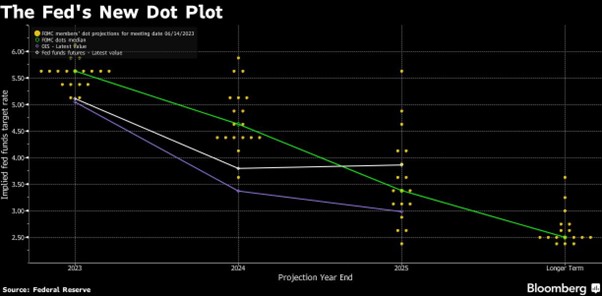

Amid these economic developments, the Federal Reserve made the decision to keep interest rates unchanged, opting to assess the impacts of the previous 10 hikes. The positive inflation data likely helped investors absorb a somewhat hawkish outlook from Fed policymakers. On Wednesday, officials announced that the official federal fund’s target rate would remain steady within the 5.00% to 5.25% range. However, the rate projections indicated by the “dot plot” suggested that this decision was more of a temporary “skip” rather than a long-term “pause,” as the median projection indicated the possibility of two additional quarter-point rate hikes by the end of the year.

The UK economy showed signs of recovery with a 0.2% sequential growth in April, following a contraction of 0.3% in March, driven by increased output in consumer-facing services, car sales, and education. This, combined with stronger-than-expected labour market data, including a 7.2% annual average wage growth and a decline in the unemployment rate to 3.8%, supported market expectations that the Bank of England (BoE) would continue its plan of raising interest rates in July. BoE Governor Andrew Bailey acknowledged the tightness of the labour market and expressed his belief that although inflation would eventually decrease, the process would take longer than initially anticipated.

In the Eurozone, industrial production rebounded more than anticipated in April, showing resilience after a decline in March, according to data released by Eurostat. The surge in output of capital goods, such as buildings and equipment, offset the reduced production of consumer goods. The eurozone experienced a notable 1.0% month-on-month increase in industrial production, resulting in a 0.2% year-on-year rise, surpassing economists’ expectations of 0.8% monthly and annual increases. Notably, capital goods output witnessed a remarkable 14.7% month-on-month increase, reversing the previous month’s 15.2% decline. However, the production of durable consumer goods declined by 2.6%, and non-durable goods saw a 3.0% decrease during the same period.

Concurrently, the European Central Bank (ECB) raised its key deposit rate to 3.5%, reaching its highest level in 22 years. ECB President Christine Lagarde expressed the view that further tightening of borrowing costs may occur in July unless there are significant changes in the economic outlook. The ECB also revised its inflation forecasts upward, supporting the case for continued monetary tightening, while reducing its projections for economic growth. Additionally, as part of its strategy to reduce its balance sheet, the ECB confirmed the cessation of reinvestments from its asset purchase program starting in July.

China’s economy encountered challenges in May as industrial output and retail sales growth fell short of expectations, further raising concerns about the stability of the post-pandemic recovery. The slowdown in economic momentum during the second quarter has prompted China’s central bank to implement its first key interest rate cuts in almost a year, indicating the need for additional measures to support the economy. Industrial output grew by 3.5% in May, slower than the previous month and below analysts’ expectations, reflecting manufacturers’ struggles with weak domestic and international demand. Similarly, retail sales, a crucial indicator of consumer confidence, rose by 12.7%, missing forecasts and decelerating compared to April’s growth rate of 18.4%.

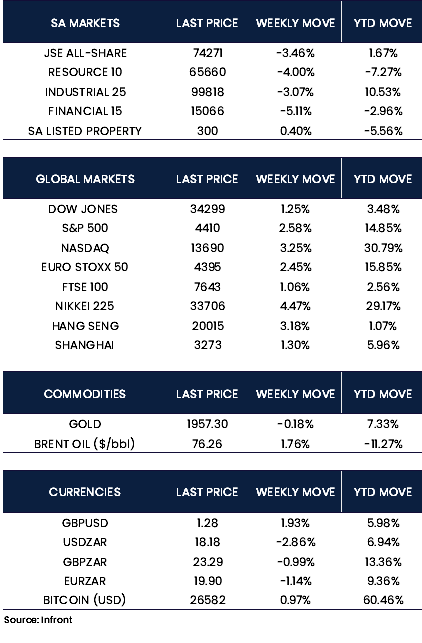

US stocks displayed a robust performance during the week, with the S&P 500 Index achieving its longest stretch of daily gains since November 2021 and its strongest weekly performance since the end of March. The tech-heavy Nasdaq surged by +3.25% over the week, while the S&P 500 and the Dow Jones also exhibited significant gains of 2.58% and 1.25% respectively. In Europe, both the Euro Stoxx 50 and FTSE 100 closed the week positively, registering gains of +2.45% and +1.06% respectively. Chinese stocks followed suit, driven by expectations of additional stimulus measures to support industries experiencing a slowdown in the wake of the waning post-pandemic recovery. The Shanghai Composite Index climbed by +1.30%, and the Hang Seng Index saw a notable increase of +3.18%. Meanwhile, Japan’s Nikkei 225 concluded the week on a higher note, recording a weekly market movement of +4.47%. The markets’ upward trajectory, reaching their highest levels in over three decades, was reinforced by the Bank of Japan’s (BoJ’s) decision to maintain its accommodative monetary policy, a widely anticipated move.

According to recent data released by Statistics South Africa (Stats SA), retail trade-in April 2023 contracted by 1.6% compared to the same period last year. This decline follows a downwardly revised 1.5% fall in March and marks the fifth consecutive month of declining retail activity, showing the swiftest pace of contraction since June 2022. The figures also exceeded market expectations of a 1.4% decrease. Stats SA highlighted that out of the seven retail categories included in the index, five experienced a year-on-year decline. Raquel Floris, the deputy director for distributive trade statistics at Stats SA, noted that the decline was primarily driven by a decrease in general dealers and retailers in the food and non-alcoholic beverages sector.

The National Assembly of South Africa has passed new legislation that paves the way for the implementation of universal health insurance, despite concerns raised by its opponents regarding its financial sustainability and effective implementation. The National Health Insurance (NHI) Bill aims to ensure equitable access to high-quality healthcare services for all South Africans. It establishes a fund that will cover most medical treatments provided by accredited healthcare providers, with pricing determined by the government. Private insurers will only be able to cover services not included in the fund’s coverage. The funding for the new fund will be derived from general tax revenue, payroll taxes, surcharges on personal income tax, and the reallocation of funds currently allocated to tax credits for private insurers, as outlined in the bill. Nicholas Crisp, the head of the health department, addressed concerns by stating that around 8.5% of the country’s gross domestic product (GDP) is already allocated to healthcare spending, and by eliminating duplication and inefficiencies, the funding gap is not as substantial as critics of the NHI anticipated.

During the week, the JSE all-share index experienced a decline of -3.46%, primarily driven by losses in the financial sector (-5.11%), followed by the resources sector (-4.00%) and the industrial sector (-3.07%). However, the overall impact of these losses was partly mitigated by a modest increase in the property sector (+0.40%). Additionally, the rand demonstrated a slight appreciation, concluding the week at a rate of R18.18 to the dollar.

Fed maintains interest rates amid economic developments. Rate projections hint at potential future hikes.