In May, the inflation rate witnessed a notable decrease, reaching its lowest annual level in over two years, as reported by the Labor Department. The consumer price index rose by only 0.1% during the month, resulting in a decline in the annual rate from 4.9% in April to 4% in May. While there has been some easing of price pressures, core inflation, which excludes volatile food and energy prices, increased by 0.4% for the month and remained 5.3% higher than the previous year.

At the wholesale level, US inflation has also experienced a decline, falling well below its pre-pandemic average. The Producer Price Index data released by the Bureau of Labor Statistics shows a modest 1.1% annual increase for the 12-month period ending in May, a sharp drop from the 2.3% growth recorded in April. This marks the lowest annual level since December 2020, with energy and food prices playing a significant role in the decline. On a monthly basis, prices saw a 0.3% decrease, reflecting the fourth decline in six months.

Despite these fluctuations, US retail sales demonstrated resilience and growth in May, defying expectations of a decline. The Commerce Department reported a 0.3% increase in retail sales across various outlets, including physical stores, online platforms, and restaurants, compared to April. This positive trend underscores the vital role of consumer spending in fuelling the economy. While gasoline stations and miscellaneous stores experienced a decrease in sales, spending grew in other categories. Excluding gasoline station sales, retail spending showed a stronger increase of 0.6%, with building materials and gardening items experiencing the highest surge of 2.2% in May. Overall, retail sales rose by 1.6% compared to the previous year.

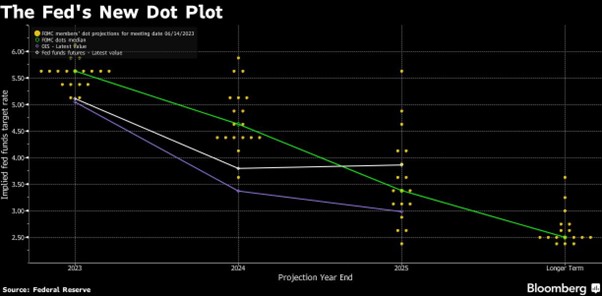

Amid these economic developments, the Federal Reserve made the decision to keep interest rates unchanged, opting to assess the impacts of the previous 10 hikes. The positive inflation data likely helped investors absorb a somewhat hawkish outlook from Fed policymakers. On Wednesday, officials announced that the official federal fund’s target rate would remain steady within the 5.00% to 5.25% range. However, the rate projections indicated by the “dot plot” suggested that this decision was more of a temporary “skip” rather than a long-term “pause,” as the median projection indicated the possibility of two additional quarter-point rate hikes by the end of the year.

The UK economy showed signs of recovery with a 0.2% sequential growth in April, following a contraction of 0.3% in March, driven by increased output in consumer-facing services, car sales, and education. This, combined with stronger-than-expected labour market data, including a 7.2% annual average wage growth and a decline in the unemployment rate to 3.8%, supported market expectations that the Bank of England (BoE) would continue its plan of raising interest rates in July. BoE Governor Andrew Bailey acknowledged the tightness of the labour market and expressed his belief that although inflation would eventually decrease, the process would take longer than initially anticipated.

In the Eurozone, industrial production rebounded more than anticipated in April, showing resilience after a decline in March, according to data released by Eurostat. The surge in output of capital goods, such as buildings and equipment, offset the reduced production of consumer goods. The eurozone experienced a notable 1.0% month-on-month increase in industrial production, resulting in a 0.2% year-on-year rise, surpassing economists’ expectations of 0.8% monthly and annual increases. Notably, capital goods output witnessed a remarkable 14.7% month-on-month increase, reversing the previous month’s 15.2% decline. However, the production of durable consumer goods declined by 2.6%, and non-durable goods saw a 3.0% decrease during the same period.

Concurrently, the European Central Bank (ECB) raised its key deposit rate to 3.5%, reaching its highest level in 22 years. ECB President Christine Lagarde expressed the view that further tightening of borrowing costs may occur in July unless there are significant changes in the economic outlook. The ECB also revised its inflation forecasts upward, supporting the case for continued monetary tightening, while reducing its projections for economic growth. Additionally, as part of its strategy to reduce its balance sheet, the ECB confirmed the cessation of reinvestments from its asset purchase program starting in July.

China’s economy encountered challenges in May as industrial output and retail sales growth fell short of expectations, further raising concerns about the stability of the post-pandemic recovery. The slowdown in economic momentum during the second quarter has prompted China’s central bank to implement its first key interest rate cuts in almost a year, indicating the need for additional measures to support the economy. Industrial output grew by 3.5% in May, slower than the previous month and below analysts’ expectations, reflecting manufacturers’ struggles with weak domestic and international demand. Similarly, retail sales, a crucial indicator of consumer confidence, rose by 12.7%, missing forecasts and decelerating compared to April’s growth rate of 18.4%.

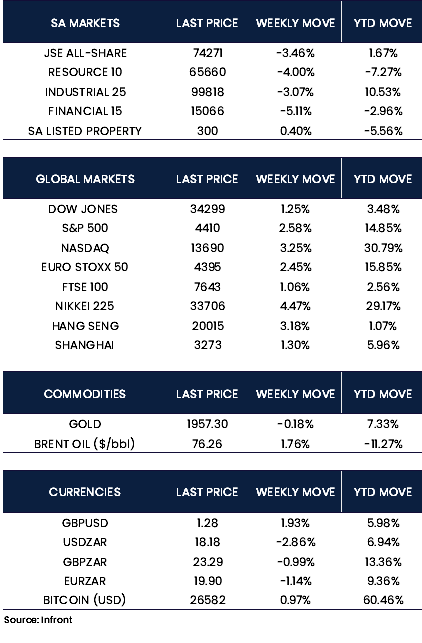

US stocks displayed a robust performance during the week, with the S&P 500 Index achieving its longest stretch of daily gains since November 2021 and its strongest weekly performance since the end of March. The tech-heavy Nasdaq surged by +3.25% over the week, while the S&P 500 and the Dow Jones also exhibited significant gains of 2.58% and 1.25% respectively. In Europe, both the Euro Stoxx 50 and FTSE 100 closed the week positively, registering gains of +2.45% and +1.06% respectively. Chinese stocks followed suit, driven by expectations of additional stimulus measures to support industries experiencing a slowdown in the wake of the waning post-pandemic recovery. The Shanghai Composite Index climbed by +1.30%, and the Hang Seng Index saw a notable increase of +3.18%. Meanwhile, Japan’s Nikkei 225 concluded the week on a higher note, recording a weekly market movement of +4.47%. The markets’ upward trajectory, reaching their highest levels in over three decades, was reinforced by the Bank of Japan’s (BoJ’s) decision to maintain its accommodative monetary policy, a widely anticipated move.

Market Moves of the Week:

According to recent data released by Statistics South Africa (Stats SA), retail trade-in April 2023 contracted by 1.6% compared to the same period last year. This decline follows a downwardly revised 1.5% fall in March and marks the fifth consecutive month of declining retail activity, showing the swiftest pace of contraction since June 2022. The figures also exceeded market expectations of a 1.4% decrease. Stats SA highlighted that out of the seven retail categories included in the index, five experienced a year-on-year decline. Raquel Floris, the deputy director for distributive trade statistics at Stats SA, noted that the decline was primarily driven by a decrease in general dealers and retailers in the food and non-alcoholic beverages sector.

The National Assembly of South Africa has passed new legislation that paves the way for the implementation of universal health insurance, despite concerns raised by its opponents regarding its financial sustainability and effective implementation. The National Health Insurance (NHI) Bill aims to ensure equitable access to high-quality healthcare services for all South Africans. It establishes a fund that will cover most medical treatments provided by accredited healthcare providers, with pricing determined by the government. Private insurers will only be able to cover services not included in the fund’s coverage. The funding for the new fund will be derived from general tax revenue, payroll taxes, surcharges on personal income tax, and the reallocation of funds currently allocated to tax credits for private insurers, as outlined in the bill. Nicholas Crisp, the head of the health department, addressed concerns by stating that around 8.5% of the country’s gross domestic product (GDP) is already allocated to healthcare spending, and by eliminating duplication and inefficiencies, the funding gap is not as substantial as critics of the NHI anticipated.

During the week, the JSE all-share index experienced a decline of -3.46%, primarily driven by losses in the financial sector (-5.11%), followed by the resources sector (-4.00%) and the industrial sector (-3.07%). However, the overall impact of these losses was partly mitigated by a modest increase in the property sector (+0.40%). Additionally, the rand demonstrated a slight appreciation, concluding the week at a rate of R18.18 to the dollar.

Chart of the Week:

Fed maintains interest rates amid economic developments. Rate projections hint at potential future hikes.