Global equity markets had a tough start to August, as Fitch Ratings unexpectedly downgraded the U.S.’s credit rating from AAA to AA+. This marked the second credit downgrade in U.S. history, raising concerns about the country’s fiscal outlook and highlighting ongoing fiscal challenges worldwide. While the impact on financial markets may be limited, it remains an important development.

U.S. employment data was in the spotlight this week, with data showing that 187,000 jobs were added in July, similar to June’s figures. This suggests that the pace of job growth has slowed compared to earlier months, where an average of 287,000 jobs were added per month in the first half of the year. The unemployment rate declined slightly to 3.5%, and wages grew by 4.4% year-on-year, indicating that the U.S. labour market is cooling just enough, adding more support to a possible soft landing for the world’s largest economy.

Other U.S. economic indicators were mixed in July, with some meeting expectations and others falling short. The eurozone, on the other hand, saw a surprising 0.3% growth in Q2, exceeding expectations. Inflation in the euro area slowed to 5.3% in July but remained well above the European Central Bank’s target of 2%.

The Bank of England (BoE) raised its key interest rate to 5.25%, the highest in 15 years, with plans to keep rates high to combat inflation. The BoE’s economic growth estimates for this year and the next remained at 0.5%. However, the UK housing market faces challenges with falling house prices and the first quarterly decline in net mortgage lending since 1987.

China experienced a decline in its manufacturing PMI, signalling contraction, while home sales faced setbacks. However, the services PMI showed growth, highlighting resilience in the services sector. In Japan, the unemployment rate improved, together with services PMI, but the manufacturing PMI fell below expectations.

In other news, heads of state from BRICS nations are set to discuss the enlargement of the group. Twenty-two nations have asked formally to become full-time members of the group, and more than 20 others have submitted informal requests. China seeks rapid expansion, while India and Brazil have concerns about the rules and potential repercussions on international relations.

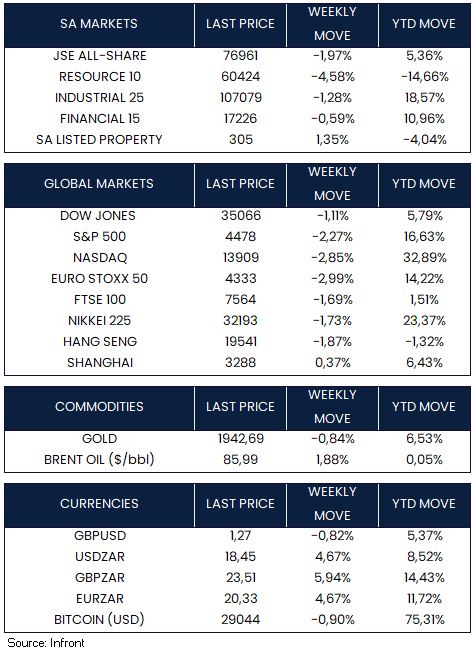

Global equity markets concluded the week with losses. In the U.S., the Dow Jones (-1.11%), S&P 500 (-2.27%), and Nasdaq (-2.85%) all closed the week in the red. Similarly, European and Asian markets, including the Euro Stoxx 50 (-2.99%), FTSE 100 (-1.69%), Nikkei 225 (-1.73%), and Hang Seng (-1.87%) indices, experienced declines, with the Shanghai Composite Index (+0.37%) being the exception.

Market Moves of the Week:

South Africa’s trade balance saw a sharp decline in June, shifting from a surplus of R9.58bn in the previous month to a deficit of R3.54bn. This was mainly driven by a significant drop in exports, contributing to a projected widening of the overall current account deficit from 1.0% of GDP in Q1 to 2.7% of GDP in Q2.

New vehicle sales saw a year-on-year improvement of approximately 1% in July, with 43,389 units sold compared to 42,822 units in July 2022. The overall trend for the past three months showed a positive growth of 8% year-on-year in total new vehicle sales, driven by strong performance in the light and heavy commercial segments, which grew by 42% and 23% respectively.

Eskom reported a substantial increase in distributed-generation solar PV capacity, with 1.82 GW added in the first six months of the year. Installed solar rooftop PV capacity rose from 983 MW in March to 4,411.5 MW in June. However, there are concerns that the reported figures might be overstated.

The JSE All-Share Index (-1.97%) was negative this week. Weaker performances came from all three of the major indices including the resource (-4.58%), industrial (-1.28%) and financial (-0.59%) sectors. By Friday close, the rand was trading at R18.45 to the U.S. Dollar, depreciating by -4.67% for the week.

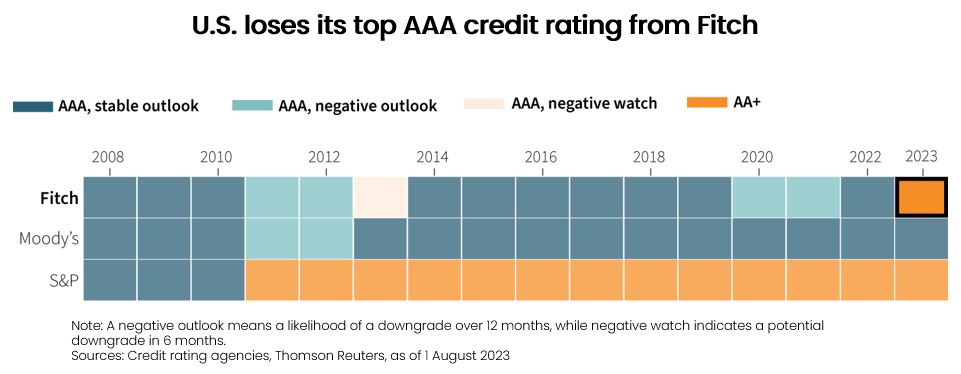

Chart of the Week:

Fitch downgraded the United States’ credit rating from AAA to AA+ on Tuesday, triggering strong reactions from the White House and surprising investors. This decision came despite resolving the debt ceiling crisis two months earlier. Fitch cited concerns about the country’s financial outlook over the next three years and the recurring last-minute debt ceiling negotiations that threaten the government’s ability to meet its financial commitments. The chart shows that Fitch downgraded the U.S.’s long-term foreign currency rating to AA+ in 2023, following a similar move by S&P in 2011.

Source: Thomson Reuters.