On Thursday, the Bank of England, implemented a 50 basis point interest rate hike (pushing the lending rate to 5%), surprising markets that had priced in a 60% chance of a 25 bps hike. Following the decision, markets saw a nearly 50% chance that Bank Rate would peak at 6.25% by the end of this year. The move comes after U.K’s May inflation figure was published on Wednesday, which showed that inflation in the region remains stubbornly high, with core inflation rising to its highest level since 1992. Headline inflation defied predictions, coming in at 8.7% y/y vs 8.4% expected, keeping in line with April’s figure. Core inflation jumped 7.1% y/y, up from 6.8% in April. In May, the central bank forecasted that inflation would drop to just over 5% by year end and be below its 2% target in early 2025.

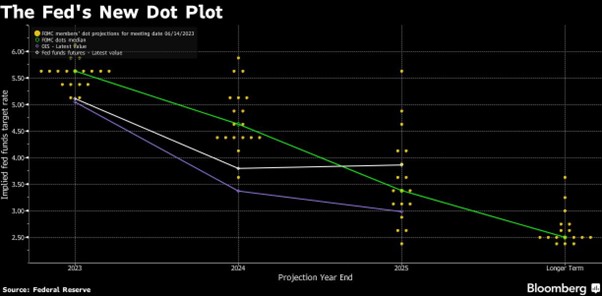

Keeping with the inflation theme, U.S. Federal Reserve Chair Jerome Powell stated this week, while addressing the Senate Banking Committee, that more rate hikes may be needed this year. Powell additionally mentioned that policymakers feel “it will be appropriate to raise rates again this year, and perhaps twice,” if the economy performs about as expected. Decisions will be made on a meeting-by-meeting basis, Powell said, while noting that there is a long way to go to get inflation back down to its 2% goal.

The latest release of flash purchasing managers index’s (PMI) data on Friday indicates a stagnation in the eurozone economy. The composite S&P Global PMI registered at 50.3. The manufacturing index declined from 44.8 in May to 43.6, while the services measure experienced a significant monthly deterioration, dropping from 55.1 to 52.4, which is an unusually substantial decrease.

On Saturday, Russian President Vladimir Putin made a firm commitment to mete out consequences to those responsible for an “armed uprising” following the apparent insurrection led by the head of the Wagner private military group – which threatened to end Putin’s 24-year rule. The insurrection involved taking control of military installations in two Russian cities, namely Rostov-on-Don and Voronezh, and included a warning that the troops could advance towards Moscow. In a sudden change of direction, Yevgeny Prigozhin, the leader of Wagner, announced that he had halted the advance of his troops towards Moscow and issued orders for them to evacuate Rostov. As part of a negotiated agreement facilitated by Belarus, Prigozhin agreed to depart from Russia and relocate to Belarus. In a statement, Prigozhin said that he wanted to avoid the spilling of “Russian blood”.

This week, the yen continued to depreciate against other major currencies, crossing the 143 mark against the dollar, coinciding with Japan’s announcement of its highest core inflation rate since 1981, standing at 4.1%. While other central banks adopted a more hawkish stance, the Bank of Japan maintained its super loose monetary policy approach. If the yen experiences further decline, it may necessitate adjustments to the Bank of Japan’s yield curve control policy.

No major indicators were released in China during the week. However, mounting evidence that the country’s recovery is losing steam raised fresh concerns about the economic outlook. China’s People’s Bank of China was the lone major central bank to lower rates this week, cutting the important loan prime rate 0.1% to 4.2% in an effort to lower borrowing costs and boost confidence and consumption.

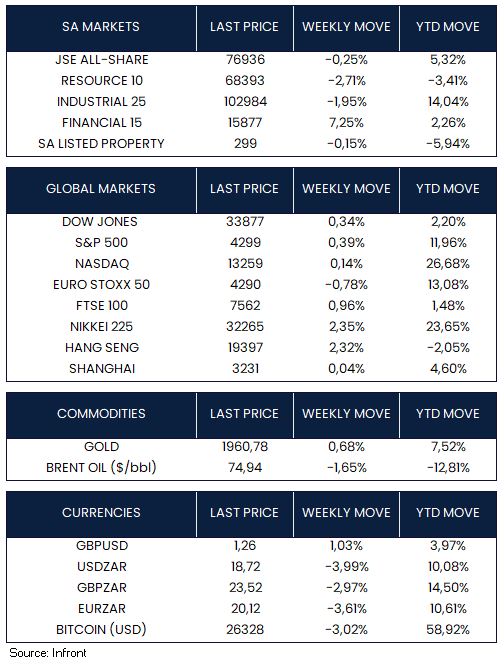

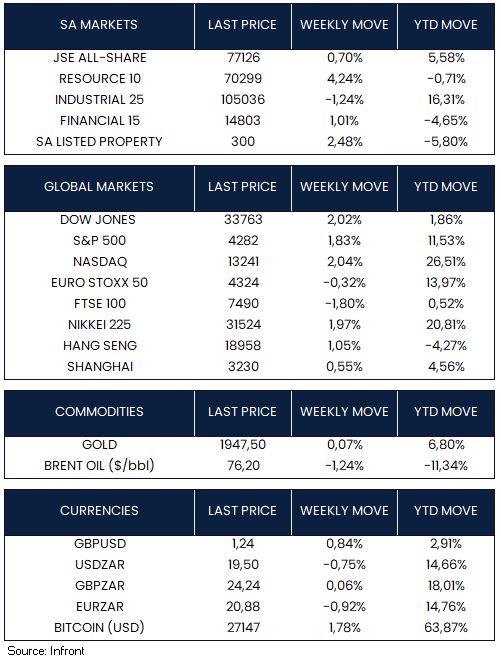

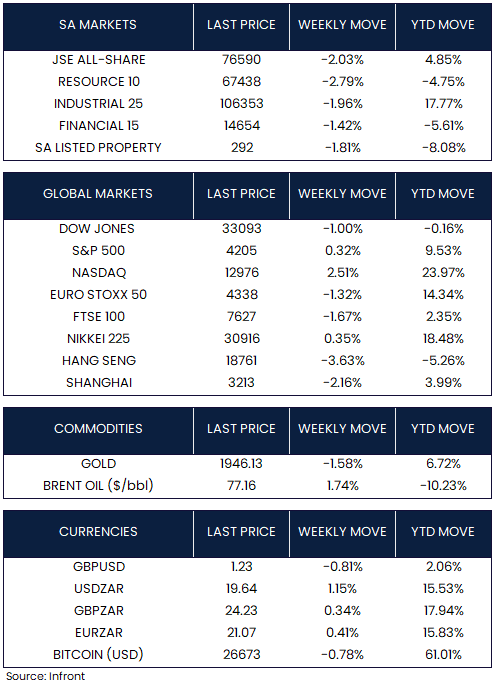

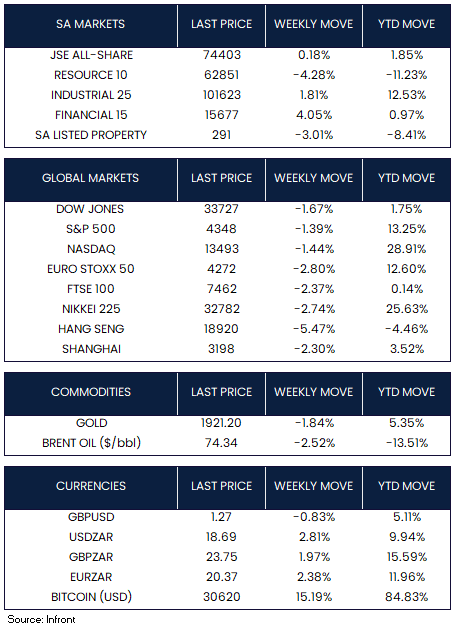

On the market front, global indices ended the week in the red. Growth stocks outperformed value shares, while large-caps fared better than small-caps. The S&P 500 Index fell -1.39%, while the Dow Jones slipped -1.67%. The technology-heavy Nasdaq Composite had a strong start to the week but ended the week down -1.44%. Shares in Europe (Euro Stoxx 50, -2.80%) and the UK (FTSE 100, -2.37%) fell over the week on worries that further interest rate increases might cause a recession in Britain and the eurozone.

Chinese shares (the Shanghai index) ended the week down -2.30%, while in Hong Kong, the benchmark Hang Seng Index declined -5.74%, its largest drop in three months. In Japan, the Nikkei 225 fell -2.74%. Gold dipped -1.84% while Brent Oil declined by -2.52% over the week.

Market Moves of the Week:

Inflation in South Africa moderated and surprised to the downside in May, with headline inflation falling to 6.3% y/y (expectations: 6.5% y/y) from 6.8% y/y in April. Importantly, the inflationary impact of food and non-alcoholic beverages, which had been a major contributing factor in the recent months, was considerably lower than expected – coming in at 11.8% y/y vs April’s 13.9% y/y print. Last year’s high fuel price also fell out of the index’s base, improving the figure. The annual rate for fuel decreased to 3.5% from 5.0% in April. Core inflation also edged lower to 5.2% y/y, as expected. Moving forward, although inflation is starting to exhibit noticeable signs of decreasing, it remains above the South African Reserve Bank’s (SARB) target range of 3%-6%.

Given the downside surprises in inflation in the past two months, the strengthening of the rand and a decline in oil prices, the inflation outlook has improved. The market is gaining confidence that the SARB has completed its hiking cycle (staying on hold in July – the next Monetary Policy Committee meeting). However economists have not ruled out further hikes, saying this would depend on the course of load-shedding and the rand’s behaviour.

According to a statement from the South African presidency, Invest International, a company owned by the Netherlands finance ministry and state development bank FMO, has committed €300 million ($330 million) to establish a public infrastructure fund for investing in water and energy projects in South Africa. The funding will be provided through a combination of €200 million in loans and €100 million in grants.

Eskom is making progress in its efforts to restructure and operationalize its transmission company by November’s end. This is part of a comprehensive plan to improve the financial and operational performance of the financially struggling power utility. Eskom’s acting group CEO, Calib Cassim, informed members of parliament that two critical requirements remain for the successful spin-off of the transmission company. These include obtaining the transmission license from the National Energy Regulator of SA (Nersa) by the end of July and securing the consent of lenders, which is expected to be achieved by the end of August.

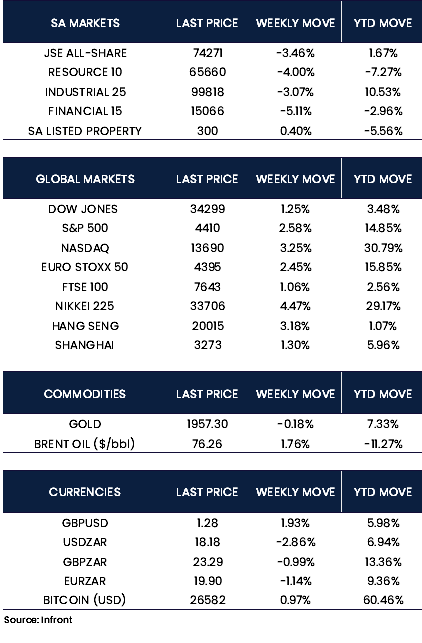

The JSE (+0.18%) managed a marginal gain over the week. Sectors were mixed with Resources selling off (-4.28%) and Financials rallying (+4.05%). The local currency weakened against the U.S. dollar over the week, rising to R18.69/$ from last week’s R18.18/$ level.

Chart of the Week:

The persistence of the country’s cost-of-living crisis, with U.K. CPI the highest in the G7, will be a headache for the government. Prime Minister Rishi Sunak promised to halve inflation by the end of this year ahead of a general election in 2024.

Source: Reuters, CNBC