Consulting Services

for Advice you can Trust

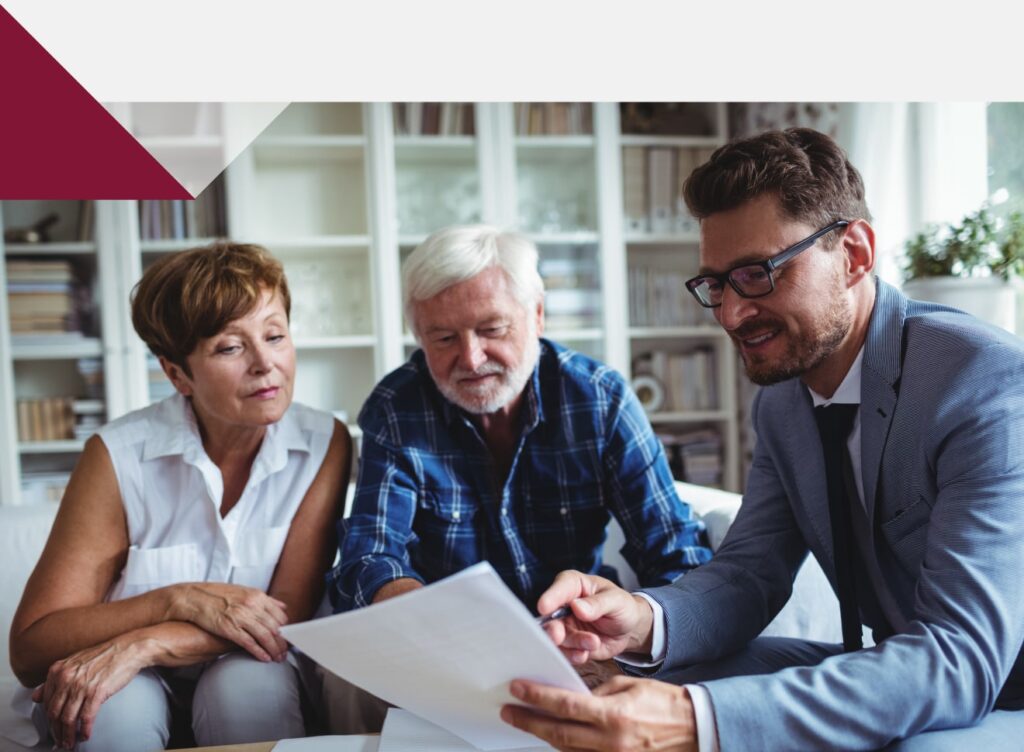

Carrick Consult provides fiduciary and financial services with the greatest care and professionalism. You will be in good hands with our team of specialist attorneys, accountants and tax practitioners.

Fiduciary Services

Preserve your wealth for generations to come by looking at the complete picture and planning diligently. Our four-silo approach to estate planning enables a 360-degree view of our clients’ wealth and the structures in which their wealth is preserved. This forms the basis around which our service offering has been designed.

Trusts are commonly used by families for estate planning purposes as it serves as a vehicle in which assets can be managed for the benefit of generations to come.

There are very strict rules contained in our legislation that apply to trusts, including; how trusts are managed, how beneficiaries are added or removed, and how trust deeds are amended. This makes it essential to have a well-drafted trust deed in place and trustees that are familiar with trust legislation and the administration of trusts.

All inter vivos trusts should have a professional, independent trustee onboard, and be carefully administered, with the aim of avoiding adverse tax and legal consequences.

Our services in the trust silo include:

- Drafting and registering new trusts

- Inter vivos (family) trusts

- Public benefit organisation trust (charitable trusts)

- Employee share trusts

- Bottom Drawer Trust / Dormant Trust

- Professional independent trusteeship

- Trust administration

- Trust amendments – trustees, trust deeds

- Trust audits

- Termination of trusts

- The MyLnD™ Programme

A liquidation and distribution account (L&D) is a written account of the process of collecting and realising the deceased’s assets, the discharge of debts, costs and taxes, and the handing over of what is left to the heirs.

On average, the administration of a deceased estate takes six to 13 months to finalise, before the heirs see the first cent of their inheritance. In large or complex matters, winding up the estate may be delayed by several years. As the only person with the full knowledge to shed light on such cases is no longer present, successful transfer of wealth to the next generation fails.

To overcome this stalemate situation, we offer the MyLnD™ Programme, which pre-empts the process of administering your future deceased estate and the transfer of your wealth to your heirs, while you are still alive. In this manner, the planning process and the administration process become a unified planning event, pro-actively preparing for the eventuality of death.

- Drafting of Wills

We provide Will drafting services to ensure that your intentions and wishes are properly recorded for the protection of both your estate and beneficiaries.

We will also advise whether you require one worldwide Will or whether a foreign Will is best suited to deal with assets in a particular jurisdiction. This depends on several factors; how many jurisdictions your assets are situated across, the laws of those jurisdiction(s) and the size and nature of your assets in a particular foreign jurisdiction.

Leaving behind a clear and valid Will is a final kindness to your loved ones, by simplifying the division and winding up of your deceased estate while they grieve.

- Estate administration

Your nominated executor needs to ensure that your estate is distributed as per the wishes in your Will. This might sound simple, but it includes closing accounts, selling and or transferring of assets, tax compliance, payments, correspondence with various parties like family members, creditors, etc.

We have professionally qualified persons who will ensure that your estate is administered in terms of the law and in a timely manner.

As part of the process of protecting your business assets and guiding your corporate affairs, having the correct contracts in place is vital to protect you and your business when disputes arise. If you are part of a company, we strongly recommend you ensure there are sound documents governing your relationship as director / shareholders of the business.

We can assist with all aspects of corporate or commercial law you may require, either in your personal life or in your private businesses. We provide advice on structuring the transaction, can attend to drafting or reviewing the relevant agreement and assist in implementation.

We can assist with, amongst other things:

- Drafting or reviewing

- Lease agreements

- Loan agreements (and related security agreements)

- Service level, consultancy or employment agreements

- Sale of shares agreements

- Sale of business agreements

- Shareholders’ agreements and memorandums of incorporation

- Supply and distribution agreements

- Privacy and data protection terms and conditions

- Software development or licensing agreements

- Conveyancing (property transfer and private bond registrations)

- Advising on and implementing

- Mergers and acquisitions

- Funding transactions

- Employee ownership plans or structures

- Dispute resolution – through formal mediation

- Life Cover

Life and disability cover fill the gap between what a person has at a certain stage in life and what would be required to ensure that the person or the person’s family is financially well looked after.

Life cover also plays a role in funding buy-and-sell obligations on death, as it provides liquidity for debt repayment on death (including debt for which the deceased stood surety) and lastly, it provides for liquidity in an estate to cover costs or estate duty.

The proceeds of life cover are included for estate duty purposes in the estate of the person whose life was insured unless certain exclusions apply.

- Pension, Provident and Annuity Policies

Governments around the world understand the value of having the older generation in their community being able to look after themselves after their working lives. To enable saving for life after work, most countries provide tax benefits on 1) premiums paid into funds earmarked for consumption after retirement, 2) the gains and income earned within those funds and 3) portions of the proceeds received by the beneficiary on retirement.

From an estate planning point of view, there is nothing that needs to be done on defined benefit policies other than being cognisant of the existence of such a policy. There is no beneficiary nomination, no lump-sum payment and no estate duty or income tax consequence for the estate or for the deceased person.

A defined contribution fund, however, is a fund that is simply the accumulation of contributions made during the policy holder’s life, and the aggregate contributions and the growth thereon is paid to the policy holders through a lump sum on retirement, as well as annuity income until the fund is depleted. As there is potentially an amount left on death, the policy holder needs to appoint a beneficiary to receive the residual benefits. Those benefits can also be taken as an annuity and then this new beneficiary, in turn, needs to appoint another beneficiary until all the funds have been depleted either through lump-sum payments or annuity payments.

Any lump sum taken from these policies after the death of a policy owner or subsequent beneficiary is taxed in the last income tax return of the deceased person. There is no death duty consequence to either the lump sum or the annuity. It is not a deemed asset for estate duty purposes.

The annuity is taxed as income in the hands of the annuitant as and when the annuities are received. The fund itself usually retains the tax-free benefit of the funds that are retained.

The only relevance to a pension or annuity fund from an estate planning point of view is that the advisor needs to ensure that the beneficiary nominations, where required, are indeed in place and that the benefit of the fund is taken into consideration when calculating the relative value each heir will receive in the end.

Financial Services

Comprehensive strategies to optimise your financial affairs.

Tax compliance is a requirement of all personal tax files but can often be a challenging task with the frequent changes to tax legislation. At Carrick Consult, we ensure that you and your business is meeting current tax requirements, without any blind spots.

Keeping your accounts up-to-date, accurate and reliable, and having access to real-time financial information at any time, makes the difference between a business that is a success and one that is not.

Our services include:

- Selecting the appropriate reporting framework for each individual’s type of business

- Designing and implementing accounting systems and controls

- Capturing and recording financial data

- Preparing and discussing monthly or ad-hoc management accounts

- Compiling financial statements

- Compiling asset registers

- Performing bank reconciliations

- Performing customer and supplier reconciliations

- Assisting our clients to comply with legal requirements

Whether for a buy and sell insurance agreement or to sell your Company, sitting with a professional to understand your business and to formulate a valuation methodology is critical for all parties concerned and time well spent.

Valuation methodologies include but are not limited to:

- Discounted cash flow valuation

- Comparing the company to other businesses that have recently been sold or acquired in the

same industry and - Listed company comparable such as price/earnings multiples.

Recent Articles

Week in Review: US Growth and Inflation

Week in Review: Higher-for-Longer U.S. Interest Rates

Week in Review: Elevated U.S. CPI and Escalating Debt Levels in China

Looking for Any of these Financial Services?

Our team of specialist attorneys, accountants and tax practitioners look forward to offering you expert advice and unrivalled experience.