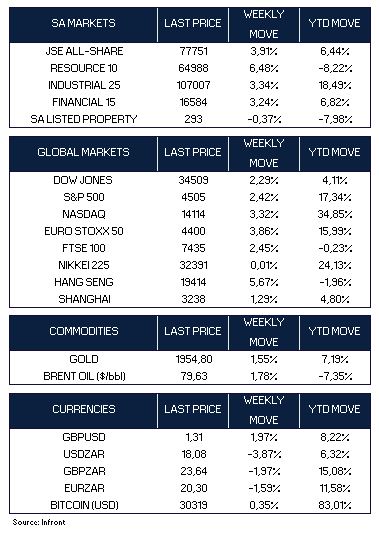

The Dow Jones Industrial Average notched its best performance since March, gaining 2.3% on the week, as lower-than-expected inflation and strong earnings results from some of the biggest banks and companies kicked off second-quarter earnings season in the US. On a weekly basis, the S&P 500 added 2.4%, while the technology-heavy Nasdaq gained 3.3%.

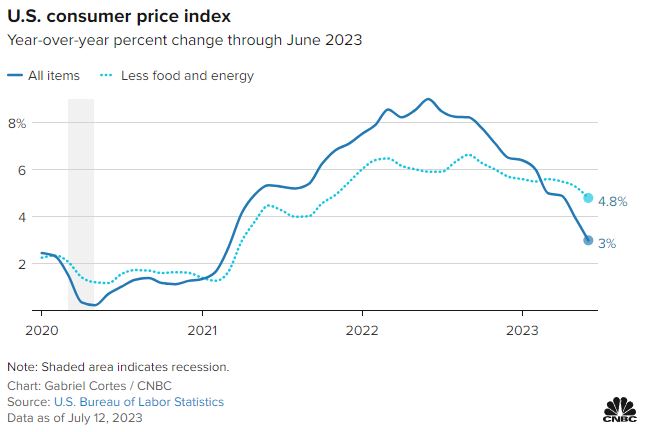

Investors’ sentiment was lifted by the soft inflation reports, with both the consumer and the producer price indexes reinforcing the notion that inflation is moderating. The Consumer Price Index (CPI) which measures inflation, increased 3% year over year, its lowest annual rate in more than two years. On a monthly basis, the index, which measures a broad range of prices for goods and services, rose 0.2%. That compared with Dow Jones estimates for respective increases of 3.1% and 0.3%.

Producer prices also rose less than expected with the producer price index (PPI), released on Thursday, showing headline producer prices rose only 0.1% over the year ended in June, nearing deflation territory.

When inflation first began to accelerate in 2021, Federal Reserve (Fed) officials thought it would be more “transitory,” but inflation has proved to be more stubborn than anticipated. The Fed began hiking, ultimately raising benchmark rates by 5 percentage points through a series of 10 increases since March 2022.

In the week ahead earnings season picks up steam in the US, with a flurry of releases from some of the world’s most prominent companies, including Elon Musk’s EV giant Tesla, as well as major banks, pharmaceutical firms, prominent airlines, tech and telecom giants.

In Europe, amidst signs of cooling US inflation, the pan-European STOXX Europe 50 Index ended the week 3.86% higher, while the UK’s FTSE Index 100 gained 2.45%.

Earlier in the week Dutch Prime Minister Mark Rutte resigned after 13 years in power after his coalition split over different approaches to immigration. Rutte, who is Europe’s second-longest serving leader, had said that his government would tender its resignation to the Dutch king, triggering new elections to be held in the fall.

In Asia, China extended support measures to the property sector, raising hopes that further support for the country’s flagging economy could be forthcoming. The Shanghai Stock Exchange Index rose 1.29% for the week, while in Hong Kong, the benchmark Hang Seng Index gained 5.71%. In a sign of weakening global demand, exports from China fell 12.4% year over year in June, the largest fall since February 2020, at the beginning of the pandemic.

Japanese equities lagged for the week, with the Nikkei 225 Index ending flat.

Oil headed for a third weekly gain as supply disruptions in Africa and a reduction in shipments from Russia tightened the market, Brent crude gained 1.78% over the week.

Gold notched its biggest weekly gain since April after signs of cooling inflation sparked hopes of a pause in U.S. interest rate hikes (higher interest rates increase the opportunity cost of holding zero-yield gold). Gold traded at $1,954 per ounce at Friday’s close, gaining 1.55% for the week.

Market Moves of the Week:

The rand was a big beneficiary of economic data this week showing cooling US inflation, driving the dollar to its weakest level since April 2022. The rand broke below R18 to the dollar for the first time in three months on Thursday and as of Friday’s close was up more than 3.8% for the week. By Friday’s close, the rand was trading at R18.08 to the U.S. Dollar.

Economic data released on Tuesday showed that the South African manufacturing sector rose 2.5% year on year after a 3.6% expansion in April. The local economy avoided a recession in Q1 when it eked outgrowth of 0.4% after contracting 1.1% in Q4 of 2022.

South Africa’s struggling utility Eskom said on Thursday that it would extend ‘Stage 6’ power cuts, its highest level on record, into the weekend as cold weather drives up demand and power station breakdowns constrain supply. Stage 6 outages mean many businesses and households are in the dark for up to 10 hours or more per day.

On the Johannesburg Stock Exchange, the broader all-share index ended the week 3.9% higher, with strong gains recorded in the resources (6.48%), industrial (3.34%), and financial sectors (3.24%).

Chart of the Week:

The Consumer Price Index (CPI) rose by less than expected, at 0.2% month over month (MoM) and a 27-month low of 3% year over year (YoY). Stripping out volatile food and energy prices, the core CPI rose 4.8% from a year ago while consensus estimates expected an increase of 5%. The annual rate was the lowest since October 2021.