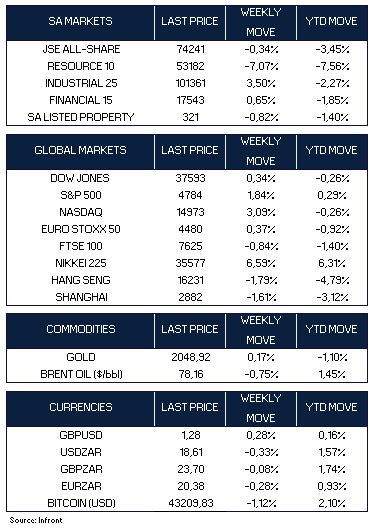

Geopolitical tensions continued to escalate in the Middle East over the week with the US and the UK carrying out multiple airstrikes on more than a dozen Houthi rebel targets in Yemen. Since mid-November Iranian-backed Houthi militants have attacked and harassed several vessels in the Red Sea and the Gulf of Aden, significantly disrupting commercial shipping in the region. Oil and gold were the main beneficiaries of the latest developments with gold ending the week at $2,048/oz, while Brent crude ended a volatile week at $78 a barrel.

There was some encouraging news on Friday on the inflation front with the unexpected fall in US producer prices by 0.1% in December, marking the third consecutive monthly decline. For 2023 as a whole, prices rose 1.0%, while core prices increased 1.8%, less than expected and below the Federal Reserve’s overall inflation target of 2.0%.

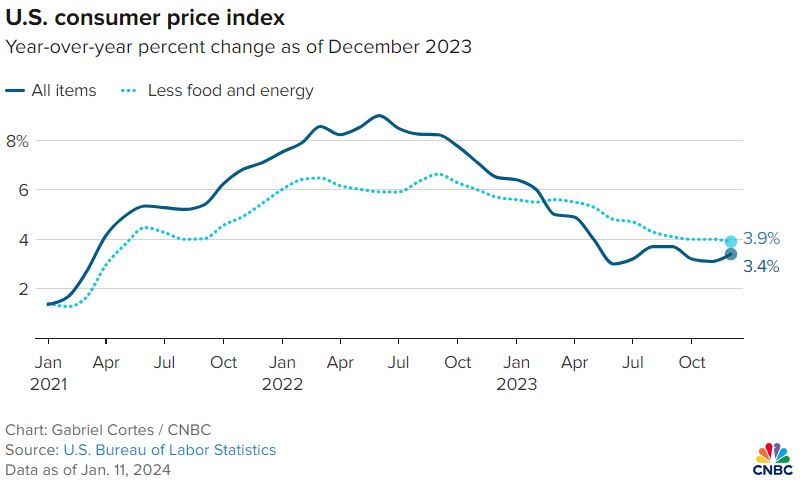

The data followed Thursdays higher than expected Consumer Price Index print, which came in modestly hotter than economists had forecasted, with prices up 0.3% on the month and 3.4% from a year ago. Core inflation (excludes volatile food and energy), meanwhile, was roughly in line with expectations, rising 0.3% for the month and 3.9% when compared to the same period the prior year.

Major US indices moved higher over the week as the 4th Quarter earnings season kicked-off in the US with some of the larger bank’s reporting. For the week the Dow Jones added 0.34%, while the S&P 500 advanced 1.84%. The Nasdaq was the outperformer, rising 3.09% over the week.

In Europe, ECB President Christine Lagarde said in an interview on Thursday that she thought “the worst part is behind us” in the battle to bring down inflation. She also asserted that interest rates had probably reached their peak and that interest rate cuts would begin once data confirmed that inflation is on a path to reach the central bank’s target. In local currency terms, the pan-European STOXX Europe 50 Index ended the week up 0.37%, while the UK’s FTSE 100 Index fell 0.84%.

Japan’s stock markets registered strong gains over a holiday-shortened week, with the Nikkei 225 Index rising 6.6% supported by continued stimulative monetary policy and weakness in the yen (boosting Japanese exports).

In contrast, Chinese equities retreated over the week with the benchmark Shanghai Composite Index declining 1.61%. Investor sentiment was impacted by the fall of China’s consumer prices for a third straight month in December, a sign of continuing weak domestic demand.

Over the weekend Taiwanese voters elected the ruling Democratic Progressive Party (DPP), which champions Taiwan’s separate identity and rejects China’s territorial claims, candidate Lai Ching-te as its next president, marking the party’s record third win in a row. In the parliamentary elections, the DPP took 51 out of a total of 113 seats, losing the parliamentary majority for the first time since 2012 and leading to a divided government for the first time since 2004. China sees Taiwan as part of its territory and Xi Jinping has made unification a goal. Saturday’s verdict will mean a continuation of the very tense situation that already exists in the Taiwan Strait.

In Crypto news, the U.S. securities regulator on Wednesday approved the first U.S.-listed exchange-traded funds (ETFs) to track bitcoin, following a decade-long tussle with the crypto industry. Following the approval, U.S.-listed bitcoin exchange-traded funds (ETFs) saw $4.6 billion worth of shares trade hands as of Thursday afternoon with the price soaring to $46,900 level. Friday saw a sharp reversal in pricing to end the week at the $43,200 level.

Market Moves of the Week

In local news, South African manufacturing production rose 1.9% year-on-year in November, whilst seasonally adjusted manufacturing sales increased by 2.1% over three months. The positive manufacturing print was supported by the release of the Absa Purchasing Managers Index (PMI) for December, a key gauge of manufacturing activity, which rose 2.7 points to 50.9.

The improved data prints will add a ray of hope to South Africa avoiding a recession (two successive negative quarters) in the fourth quarter of 2023. South Africa’s economy contracted 0.2% in the third quarter (Q3) last year.

The JSE All Share index was marginally lower on the week (-0.34%), with the resource sector sharply lower on the week, investors remain concerned around the recovery of the Chinese economy. On the currency front, dollar strength hit emerging market currencies across the board, with the rand ending the week at R18.61/$ level.

Chart of the Week

The US consumer price index, the most widely used measure of inflation rose a more-than-expected 0.3% in December from the month before after rising only 0.1% in November. On a year-over-year basis, prices rose 3.4%, up from November’s 3.1% pace. Elevated housing and auto insurance costs stood out. Excluding volatile food and energy prices, core CPI also rose 0.3% for the month and 3.9% from a year ago, marking the slowest 12-month pace since mid-2021.