As 2023 concluded, the notable nine-week winning streak in global equities ended, marked by a modest downturn attributed to early-year repositioning and a natural pause following an impressive rally in the final two months of the preceding year. Looking ahead to 2024, the key factors expected to influence performance are interest-rate decisions and the trajectory of the global economy, similar to the dynamics observed in 2023.

The holiday-shortened week focused on obtaining additional details about the Federal Reserve’s outlook on policy decisions for 2024 and the latest evaluation of the U.S. labour market. Geopolitical concerns also weighed on sentiment. Over the previous weekend, and in advance of upcoming elections in Taiwan, Chinese President Xi Jinping stated that “the reunification of the motherland is a historical inevitability.” Investors also appeared worried about a further escalation of tensions in the Red Sea, with Iran sending a warship and the U.S. sinking attacking ships armed by Houthi rebels from Yemen.

U.S. economic data releases presented mixed signals on employment. December witnessed strong job growth, exceeding expectations, and resulting in higher-than-anticipated wage gains. Despite the unemployment rate holding steady at 3.7%, the workforce participation rate unexpectedly retreated to 62.5%, reaching its lowest point since February. Additionally, the ISM’s Non-Manufacturing Employment Index sharply declined, entering contraction territory, and reaching its lowest level since July 2020.

An upturn in inflation within the eurozone in December seemed to diminish the likelihood of early rate cuts by the European Central Bank. A preliminary assessment suggested that the annual consumer price growth increased to 2.9% from a two-year low of 2.4% in November, primarily influenced by a reduction in government subsidies for electricity, gas, and food. However, a gauge of core inflation, excluding the more volatile food and energy costs, declined to 3.4% from 3.6%.

The economic repercussions of the January 1 earthquake in Japan involves infrastructure damage, threatening manufacturing and supply chains, with the affected region hosting semiconductor-related factories. Initial estimates suggest a limited macroeconomic impact despite ongoing evaluations. BoJ Governor Kazuo Ueda reassured comprehensive central bank support for the financial system post-disaster.

China’s Caixin services PMI exceeded market expectations in December, driven by increased new business, leading to a three-month high in sector optimism. In contrast, China’s property market exhibited further signs of decline, with new home sales by the top 100 developers dropping by 34.6% in December compared to the previous year, exacerbating concerns about the impact on the country’s economy.

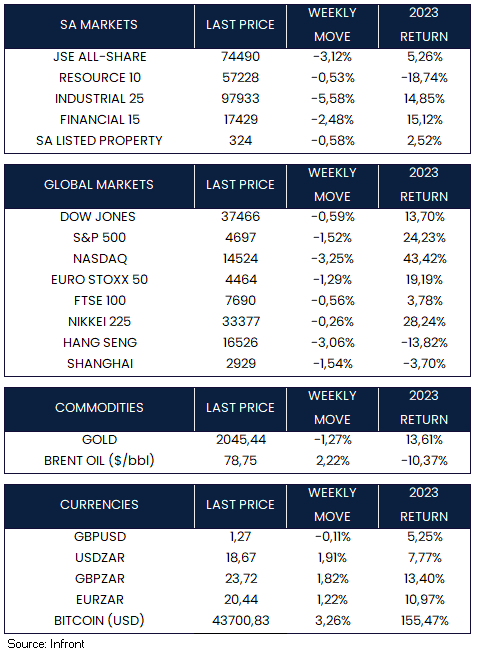

The beginning of 2024 saw a subdued performance in a trade shortened week. In the U.S., the Dow Jones (-0.59%), S&P 500 (-1.52%), and Nasdaq (-3.25%) all exhibited weakness. Correspondingly, European and Asian markets generally experienced declines, with negative movements observed in the Euro Stoxx 50 (-1.29%), FTSE 100 (-0.56%), Nikkei 225 (-0.26%), Hang Seng (-3.06%), and Shanghai Composite (-1.54%) indices.

Market Moves of the Week

The power situation in South Africa is precarious, with Eskom having approximately R3.6 billion left in its diesel budget for the 2023/2024 financial year, concluding on March 31, 2024. With an average monthly spending of R3 billion on diesel this year, depletion of the diesel budget before the fiscal year ends is anticipated. Eskom’s diesel expenditure has more than doubled compared to the same period last year, reaching R24.3 billion as of November 28, highlighting the escalating costs and challenges in maintaining the power supply in South Africa

Meanwhile, President Cyril Ramaphosa has finally reshaped the responsibilities of Minister of Electricity Kgosientsho Ramokgopa, transferring the crucial task of procuring new electricity generation from Minerals and Energy Minister Gwede Mantashe, who encountered challenges in this domain. This change provides clarity to Ramokgopa’s role, which was previously undefined since his appointment in March.

In line with global market trends, the JSE All-Share Index (-3.12%) opened 2024 on a weaker note, with notable declines across all three major sectors including the resource (-0.53%), industrial (-5.58%), and financial (-2.48%) sectors. By the close of Friday, the rand was trading at R18.67 to the U.S. Dollar.

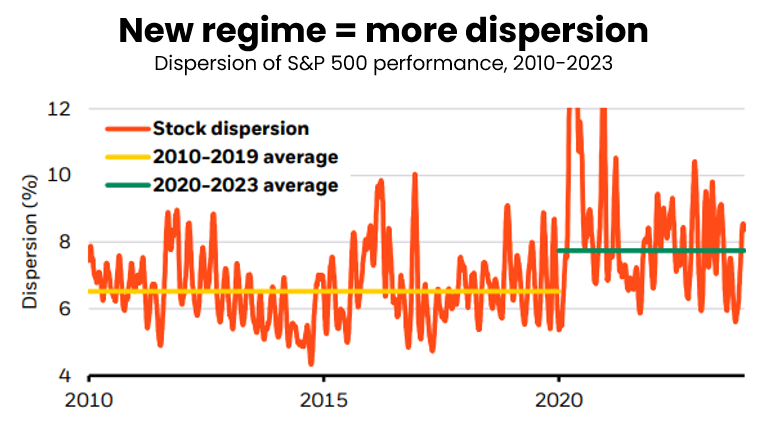

Chart of the Week

In 2023, equity markets rebounded sharply, driven by technology stocks. The chart shows a widening gap in individual stock returns since 2020 (green bar), reflecting heightened volatility due to macro uncertainty, geopolitical factors, and structural shifts. The influence of artificial intelligence on U.S. stocks highlights the significance of current mega forces, shaping the market landscape beyond future trends. Source: BlackRock Investment Institute, with data from LSEG Datastream.