Global equity markets experienced positive momentum during the week, buoyed by steady interest rate decisions and better-than-expected U.S. GDP growth. The Dow Jones Industrial Average and the S&P 500 Index both achieved new all-time highs, with the latter marking its 12th weekly advance out of the last 13 weeks.

U.S. GDP growth for the fourth quarter of 2023 exceeded expectations, driven by stronger-than-expected consumer spending. Preliminary estimates released on Thursday indicate a 3.3% annualised growth rate for the quarter. The overall economic expansion for 2023 stood at 2.5%, primarily fuelled by a 2.8% increase in personal spending throughout the year. Business and household investment also contributed to an above-forecast growth in the final quarter.

In US political news, former President Donald Trump secured another victory in the New Hampshire primary, strengthening his position as the likely Republican party nominee. This win comes after a decisive victory in Iowa and poses a setback to his major rival, Nikki Haley, ahead of the upcoming primary in South Carolina on Feb. 24. Additionally, Trump testified in a US court as part of a defamation case brought by Jean Carroll, relating to allegations of sexual assault in the 1990s.

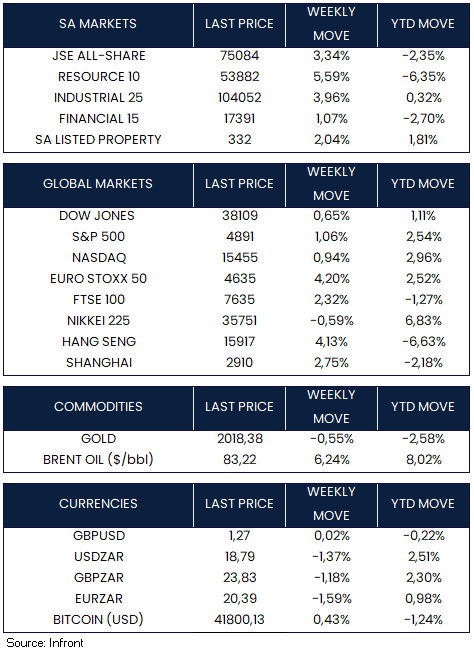

The Dow Jones Industrial Average ended the week up 0.65%, followed by the tech heavy NASDAQ composite up 0.94%. The S&P 500 was the standout performer in the U.S. closing the week at 4891 points, a weekly move of 1.06%.

In the UK, the consumer confidence gauge reached its highest level in two years in January, buoyed by slowing inflation, which increased optimism among households. Business activity in the country exceeded expectations in January, as reflected in the preliminary S&P Global/CIPS UK composite PMI, which rose to 52.5, marking the highest level in seven months, up from 52.1 in December. However, disruptions in shipping along the Red Sea led to rising input prices in the manufacturing sector, the first increase since April, potentially contributing to a pickup in inflation. The FTSE 100 advanced over the week, closing up 2.32%.

As expected, the European Central Bank (ECB) maintained its borrowing costs for the third consecutive meeting, with the deposit rate to stay at 4%. The focus is on how long the rates will remain unchanged, with President Christine Lagarde and other ECB officials suggesting that a reduction in interest rates is likely around mid-2024. Lagarde’s recent comments have led markets to speculate that earlier rate cuts might be on the table. Traders are now pricing in a 90% chance of a reduction in April and anticipating a total easing of 141 basis points throughout the year, up from the previous estimate of 130 basis points. Importantly, the ECB has stated that they will remain data dependent and not time dependent. The Euro Stoxx 50 responded positively to these developments, closing the week up 4.20%.

Contrary to other developed market peers, Japanese government bonds experienced a drop as traders interpreted comments from the central bank as hawkish, prompting them to advance their expectations for an interest rate hike in the coming months. The yield on the benchmark 10-year notes rose by 10.5 basis points to 0.74%, marking the highest level in over a month. Governor Kazuo Ueda’s statements, indicating increased certainty in achieving the Bank of Japan’s price projections, align with the prevailing expectation among economists that the BOJ might raise rates in the first part of this year. In economic data, Tokyo’s new core CPI (excluding fresh food and energy) for January recorded a year-on-year increase of 3.1%, indicating a slowdown from the 3.5% figure in December 2023 and falling below the market forecast of 3.4%. The Nikkei 225 was the only major global equity market to close the week in the red, ending down -0.59%.

Chinese equities experienced gains following powerful stimulus measures implemented by Beijing to support the economy. The Shanghai Composite Index rose by 2.75%, and the blue-chip CSI 300 saw a gain of 1.96%. Meanwhile, in Hong Kong, the benchmark Hang Seng Index recorded a notable advance of 4.13%. The People’s Bank of China (PBOC) has announced comprehensive plans to channel funds into strategically important sectors to stimulate the economy, following an unusual move related to the reserve requirement ratio (RRR). Economists anticipate that the PBOC will guide credit toward specific areas, implement slight reductions in the reserve requirements for banks, and introduce modest policy-rate cuts. In terms of data, China reported record highs in coal production and imports for December. Additionally, the country experienced a surge in imports of chipmaking machinery in 2023, reaching almost $40 billion, as firms increased investments to counteract efforts to hinder China’s semiconductor industry led by the United States.

Market Moves of the Week

In South Africa, the Reserve Bank’s Monetary Policy Committee (MPC) decided to maintain the repo rate at 8.25%, marking the fourth consecutive meeting without a rate change. The prime lending rate also remains steady at 11.75%. The SARB has increased rates by a cumulative 475 basis points since late 2021. The newly appointed MPC member, David Fowkes, replaces Kuben Naidoo, who resigned in the previous year.

South African Consumer Price Index (CPI) figures for December revealed a cooling headline inflation rate of 5.1%, compared to 5.5% in November. Governor Lesetja Kganyago emphasized that inflation needs further improvement to align with the 4.5% anchor point for policy adjustments. Core inflation, excluding food and energy, remained at 4.5%, consistent with November. GDP growth forecasts for 2024 and 2025 remained unchanged at 1.2% and 1.3%, respectively.

Former President Jacob Zuma was dealt a double blow this week. Mr Zuma faces legal action to repay nearly R29 million in legal fees for his corruption trial defence, following a Supreme Court of Appeal ruling two years ago. Additionally, the Independent Electoral Commission confirmed that Mr Zuma doesn’t meet the requirements to register as a candidate in the upcoming elections.

On the local equity front, the JSE ALSI caught the tailwinds of global markets, strongly advancing over the week, up 3.34%. All sectors positively contributed to the overall market performance, with Resources leading the market higher with a 5.59% return over the week. The risk on environment was positive for the ZAR, appreciating 1.37% against the Dollar, closing the week at R18.79/$.

Chart of the Week

The semiconductor sector, led by companies like Nvidia Corp., is currently in a favourable position, benefiting from a surprising geopolitical development. Despite initial concerns before Taiwan’s election, where the newly elected president favours independence from China, the outcome has brought calm and seemingly maintained the status quo. This stability is particularly impactful for share prices in the semiconductor industry, influencing indices such as the U.S. Philadelphia Stock Exchange Semiconductor Index (SOX), European company ASML Holding NV, and Taiwan Semiconductor Manufacturing Co.

Source: Bloomberg.