Financial markets got off to a quiet start this week, as investors awaited the release of the U.S. consumer inflation data on Tuesday. While CPI for February met expectations at 0.4% (MoM), core prices exceeded forecasts, primarily due to rising shelter costs. On Thursday, producer inflation surprised on the upside, causing concerns about potential consumer price impacts.

Interestingly, the U.S. stock market’s reaction to inflation was tempered by weaker-than-expected retail sales data on Thursday. Despite a 0.6% rise in February retail sales, the increase was driven by higher gasoline prices, while online sales declined, indicating a potential slowdown in consumer spending. The bond market reacted more strongly to the inflation surprises, with the 10-year Treasury note reaching its highest intraday level of 4.32% since February.

Looking ahead, the Federal Reserve’s reaction to inflation data will be crucial, especially with the next meeting approaching. While investors anticipate rate cuts from June, there’s debate over the extent of the Fed’s response.

On the economic front, Biden unveiled a $7.3 trillion fiscal budget proposal, focusing on middle-class tax breaks and enhanced services, funded by higher taxes on the wealthy and corporations.

Meanwhile, in U.S. politics, Donald Trump secured the Republican presidential nomination, setting the stage for a contentious rematch with President Joe Biden. Trump’s return to the political arena is expected to impact various sectors, intensifying market scrutiny.

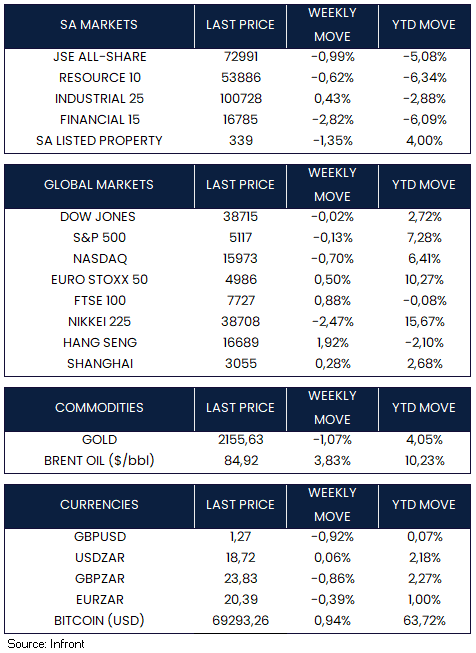

U.S. equities experienced slight declines for the week, with investors assessing unexpected increases in inflation figures alongside indications of tempered consumer spending. The Dow Jones Industrial Average fared better compared to other major indexes, achieving a record peak on Wednesday before retracting to finish the week nearly unchanged at -0.02%. Meanwhile, the S&P 500 and Nasdaq both recorded declines, down by -0.13% and -0.70% respectively.

The ECB has introduced a new framework for monetary policy implementation, maintaining the current interest rate steering system while granting lenders greater control over their cash needs. This adjustment aims to support the ECB’s primary goal of ensuring stable prices across the 20-nation eurozone. Under the revamped system, banks will determine their required liquidity, in addition to funds provided through a new permanent bond portfolio.

In response to economic conditions, ECB policymakers are considering rate cuts to lower borrowing costs. Governing Council member Yannis Stournaras emphasised the importance of initiating rate cuts soon to prevent monetary policy from becoming overly restrictive.

Among ECB policymakers, Francois Villeroy de Galhau, Robert Holzmann, and Pierre Wunsch have advocated for potential interest rate cuts by June. This comes as eurozone industrial production experienced a larger-than-expected decline of 3.2% month-on-month in January, exceeding market forecasts and highlighting economic challenges in the region.

In the UK, the unemployment rate unexpectedly rose to 3.9% while wage growth fell to 6.1%, the lowest since mid-2022. However, the economy is showing signs of recovery with a 0.2% increase in GDP in January. Bank of England Governor Andrew Bailey noted the UK’s likely full employment status and expressed reduced concerns about potential wage-inflation issues.

Encouraging corporate earnings and growing hopes for a June reduction in borrowing costs by the ECB boosted European equity markets, resulting in gains for both the Euro Stoxx 50 (+0.50%) and FTSE 100 (+0.88%) by the end of the week.

The Bank of Japan (BoJ) is expected to make a historic move by ending its negative interest rate policy at its upcoming monetary policy meeting next week, signalling the first hike in 17 years. This decision reflects policymakers’ confidence in a positive cycle of wage growth and price increases, with this year’s labour-management pay negotiations expected to result in the highest average wage rises in about three decades. BOJ Governor Kazuo Ueda has highlighted the importance of achieving the central bank’s 2% inflation target alongside wage growth in guiding monetary policy adjustments.

China’s economic data displayed a mixed performance. Consumer prices increased by 0.7% year-on-year due to higher food and services costs during the Lunar New Year, while the producer price index (PPI) declined by 2.7%, indicating persistent deflationary pressures amid weak domestic demand. Despite injections of funds by the People’s Bank of China, lending rates remained steady, leading to a net withdrawal of funds. Additionally, the State Council pledged a 25% spending increase by 2027 to spur consumption and business investment. Nonetheless, China’s property market continued its decline, with new home prices falling for the eighth consecutive month.

Asian stock markets showed mixed results this week with the Nikkei 225 Index (-2.47%) experiencing losses, while its Chinese counterpart saw gains from the Shanghai Composite Index (+0.28%) and the Hang Seng Index (+1.92%).

Market Moves of the Week

South Africa’s National Assembly on Thursday passed the Electricity Regulation Amendment Bill, granting cities and towns the right to generate their own electricity, fostering competition in the energy market, a positive step in solving South Africa’s ongoing energy crisis.

Meanwhile, SA’s central bank governor expressed confidence in South Africa’s removal from an international financial crime watchdog’s “grey list” next year, citing ongoing efforts to address identified issues.

On the economic front, government terminated a deal to sell a controlling stake in its flag carrier, SAA, due to disagreements over valuation, with the SA government valuing SAA at R5bn, while the buyer was still seeking the covid-related price of R2bn. Minister Pravin Gordhan was clear that more money from the fiscus would go towards SAA.

In the financial sector, South Africa is set to license approximately 60 cryptocurrency platforms by the end of the month, making it one of the first African nations to require permits for digital-asset exchanges. The move aims to regulate the growing cryptocurrency market and enhance consumer protection.

The JSE All-Share Index ended the week lower, declining by -0.99%, primarily influenced by the downturn in resource shares (-0.62%) and financial shares (-2.82%), although industrial shares showed some resilience with a gain of +0.43%. At the week’s end on Friday, the rand closed trading at R18.72 against the U.S. Dollar.

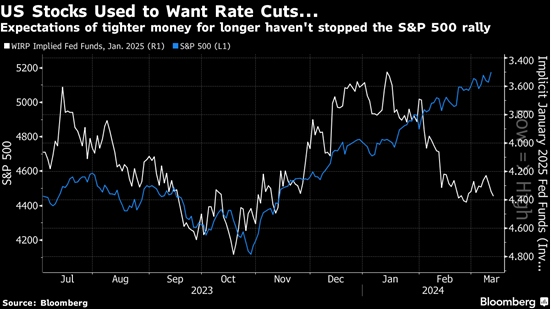

Chart of the Week

Tuesday’s core CPI print for February came in higher than expected, yet the U.S. stock market wasn’t bothered. For much of 2023, the S&P 500 moved inversely to expected fed funds rates, with the index selling off while the Federal Reserve was expected to keep rates “higher for longer”, and then surging as the central bank pivoted toward cuts. However, this year has seen a significant reduction in the number of anticipated rate cuts, and the stock market has remained unmoved. This chart, comparing the S&P 500 to the implied fed funds rate (on an inverted scale), shows a clear inverted correlation last year that has now disappeared. Source: Bloomberg