In March, U.S. employers surpassed expectations by hiring a significantly larger number of workers and increased wages. This suggests that the economy concluded the first quarter on a robust note and could potentially postpone anticipated interest rate cuts from the Federal Reserve this year. According to the Labor Department’s Bureau of Labor Statistics, nonfarm payrolls surged by 303,000 for the month, exceeding the downwardly revised 270,000 gain observed in February. Average hourly earnings rose 0.3% in March after gaining 0.2% in the prior month.

U.S. manufacturing exhibited growth for the first time in 18 months in March, with a notable resurgence in production and an uptick in new orders. According to the Institute for Supply Management (ISM), the manufacturing index rose to 50.3 in March from 48.3 in February. Conversely, growth in the U.S. services industry continued to decelerate. The ISM reported on Wednesday that its non-manufacturing Purchasing Managers’ Index (PMI) fell to 51.4 last month from 52.6 in February. This marks the second consecutive monthly decline in the index following a rebound in January.

Annual headline inflation in the eurozone decelerated beyond initial forecasts, reaching 2.4% in March compared to 2.6% in February. Similarly, core inflation, excluding volatile food and energy components, eased to 2.9% from 3.1%. However, service prices saw a sustained year-over-year increase of 4.0% for the fifth consecutive month.

Concurrently, the eurozone witnessed a notable shift as the composite Purchasing Managers’ Index (PMI) returned to positive territory in March for the first time since May. S&P Global revised its estimate for the eurozone’s composite PMI, incorporating both services and manufacturing, to 50.3, marking an increase from the initial 49.9. A reading above 50 indicates an expansion in private-sector business activity.

Minutes from the European Central Bank’s (ECB’s) March meeting revealed policymakers’ growing confidence in the timely deceleration of inflation towards target levels. While a majority acknowledged the strengthening case for rate reductions, they also emphasized the importance of awaiting key economic data scheduled to be released after the ECB’s April meeting before making any decisions.

China’s manufacturing sector experienced its most rapid expansion in 13 months, as indicated by a private survey. This growth was accompanied by a notable surge in business confidence, reaching an 11-month peak, propelled by an uptick in new orders from both domestic and international customers. The Caixin/S&P Global Manufacturing Purchasing Managers’ Index (PMI) increased to 51.1 in March from 50.9 the previous month, reflecting this positive trend.

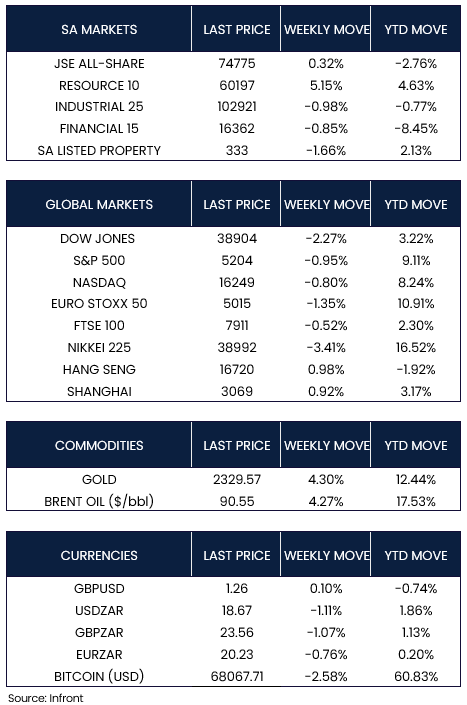

This week, global equity markets experienced a pullback from their recent highs, amid hawkish comments from some U.S. Federal Reserve policymakers and elevated crude oil prices, which raised concerns about the timing of potential interest rate cuts. In the U.S., major indices such as the Dow Jones (-2.27%), S&P 500 (-0.95%), and Nasdaq (-0.80%) all ended the week lower. Similarly, the pan-European STOXX 50 Index saw a decline of -1.35% during the shortened trading week, breaking a 10-week streak of gains. The UK’s FTSE 100 Index also saw a modest decline of -0.52%.

Japan’s stock markets also faced downward pressure, with the Nikkei 225 Index declining by -3.41% over the week.

In contrast, Chinese equities showed resilience, supported by positive economic indicators suggesting a potential acceleration in economic growth. The Shanghai Composite Index rose by +0.92%, while in Hong Kong, the benchmark Hang Seng Index increased by +0.98%.

Market Moves of the Week

South African manufacturing activity declined in March, as indicated by Absa’s latest Purchasing Managers’ Index (PMI) survey released on Tuesday. The seasonally-adjusted PMI decreased to 49.2 points in March from 51.7 in February, falling below the critical 50-point threshold that distinguishes expansion from contraction. According to Absa’s statement on Tuesday, despite significant improvements in February, both the business activity and new sales orders indices decreased in March, though they remained above the recent lows observed in January.

On Tuesday, the South African Revenue Service (SARS) announced its preliminary estimates, revealing that it had collected over R1.74 trillion during the 2023/24 fiscal year. This represents a 3.2% increase compared to the previous year’s collection. Moreover, the figure exceeds the forecast outlined in Finance Minister Enoch Godongwana’s February budget presentation to Parliament by R10 billion. Consequently, this surplus indicates a potential for a slight reduction in the Treasury’s projected budget deficit of 4.9% of gross domestic product (GDP).

During the week, the JSE All-Share Index saw a modest increase of +0.32%, largely driven by a notable surge of +5.15% in the resources sector. In contrast, the property sector (-1.66%), industrial sector (-0.98%), and the financial sector (-0.85%) ended the week with losses. By the close of trading on Friday, the rand strengthened against the U.S. Dollar, trading at R18.67, marking a weekly appreciation of +1.11%.

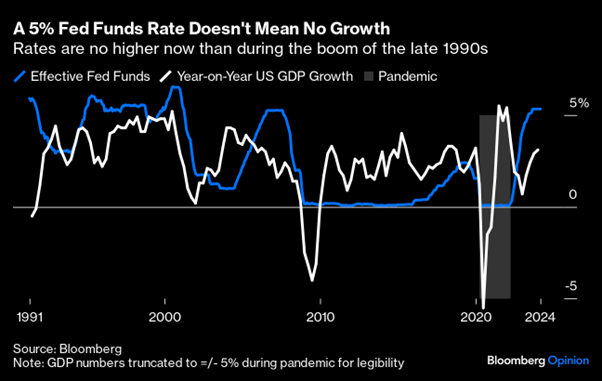

Chart of the Week

After extensive debate, the anticipated scenario of “higher for longer” has materialized. The fed funds rate reached 5% in March last year, with market expectations pricing it to remain at this level until November. While previously perceived as a concerning scenario, such elevated rates typically indicate a robust economic environment. Source: Bloomberg.