Third-quarter economic growth in the US expanded faster than expected, highlighted by a better-than-expected gross domestic product report, which showed that the U.S. economy grew at an annualized pace of 4.9% in the third quarter, led by strong consumer spending. This preliminary growth reading marked a substantial increase from the second quarter’s 2.1% pace and was the most robust figure since the fourth quarter of 2021, surpassing economists’ average prediction of 4.3%.

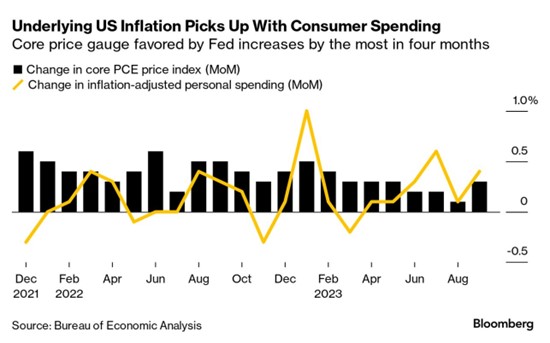

On the inflation front, the core personal consumption expenditures (PCE) price index, a measure of inflation closely watched by the Federal Reserve, presented mixed signals. The year-over-year measure slightly decreased to 3.7% in September from the previous 3.8%. Despite remaining above the Fed’s 2% long-term inflation target, it is widely expected that the central bank will maintain rates steady at its upcoming October 31-November 1 policy meeting.

It was a busy week for quarterly earnings reports, with just under half of the constituents of the S&P 500 Index having reported for Q3 2023. Investor attention was notably focused on Amazon, Alphabet (Google’s parent company), Meta Platforms (owner of Facebook), and Microsoft, members of the mega-cap technology-focused group of stocks known as the Magnificent Seven. Amazon’s report, released after market close on Thursday, appeared to receive the most positive reaction, with shares of the company rallying strongly on Friday.

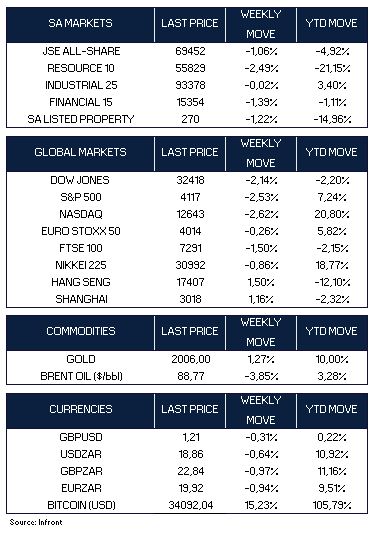

U.S. equities ended the week lower for a second straight week, as market sentiment was dented by mixed corporate earnings reports and concerns about higher interest rates. The Dow dropped by 2.1%, the S&P 500 by 2.5%, and the Nasdaq ended the week 2.6% lower.

On Wednesday, the Bank of Canada held rates steady at 5% while retaining a tightening bias, the central bank acknowledged the lagged effects of monetary policy in holding back economic activity and moderating price pressures.

In Europe, the pan-European STOXX 50 Index edged 0.26% lower due to uncertainties regarding interest rates, the economy, and conflicts in the Middle East. The UK’s FTSE 100 Index lost 1.50%.

The European Central Bank (ECB) left short-term interest rates unchanged this week, raising expectations that rates may have peaked in the eurozone. After ten consecutive rate increases, the ECB kept its key deposit rate at 4.0%. ECB President Christine Lagarde highlighted the expectation of ongoing weakness in the eurozone economy for the remainder of the year.

Japanese equities were also down by 0.86% for the week, influenced by rising bond yields and geopolitical tensions. Japan’s core inflation rate accelerated to 2.7% in October, surpassing expectations, while the consumer price index rose to 3.3% from 2.8% in September.

In China, equity markets ended the week stronger with the benchmark Shanghai Composite Index advancing 1.16% driven by increased government economic stimulus.

Amid rising concerns about escalating military action in the Middle East, the price of gold broke through the $2,000 per ounce threshold as investors sought refuge in safe-haven assets.